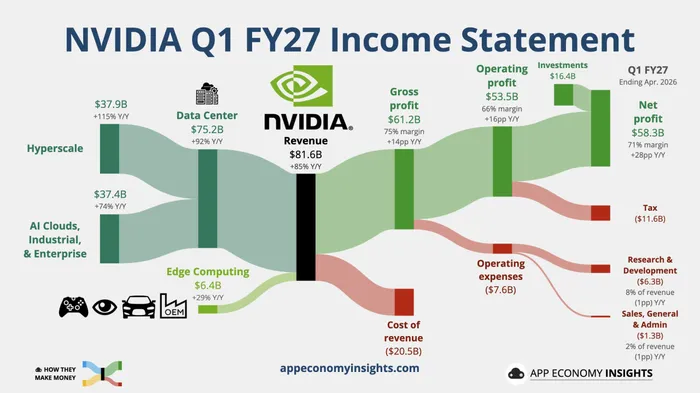

Nvidia reported first-quarter fiscal 2027 results for the period ended April 26, 2026. Revenue rose 85% year over year to $81.62 billion, about 3% above analysts' $79.2 billion estimate.

Non-GAAP adjusted EPS rose 140% year over year to $1.87, nearly 6.3% above the $1.76 consensus estimate. Gross margin reached 75.0%, higher than analysts' 74.5% expectation.

But the beat was not large enough for a stock priced for exceptional upside. Before the report, Bank of America analyst Vivek Arya's team noted that Nvidia's actual revenue had exceeded management guidance by an average of 7% to 8% over the past ten quarters. Since the prior guidance midpoint was $78.0 billion, that historical pattern implied quarterly revenue of roughly $83 billion to $84 billion. Actual revenue came in almost 1.7% below the low end of that range.

Second-quarter guidance was also strong, but not spectacular. Nvidia expects Q2 revenue of $91.0 billion, plus or minus 2%, implying a range of $89.18 billion to $92.82 billion. That is above the $87.0 billion analyst consensus, but below the most bullish estimate of $96.0 billion. Importantly, this guidance does not include China, leaving room for future upside if China-related demand returns.

The margin outlook also became a key valuation issue. Nvidia expects Q2 non-GAAP gross margin of 75.0%, plus or minus 50 basis points, or 74.5% to 75.5%. That is slightly below the prior quarter's 75.1%. The 0.1 percentage-point decline is small and does not signal clear pressure by itself, but for a company already trading at a high valuation, investors will watch closely to see whether gross margin is nearing a cyclical high. Product transitions, supply-chain expansion and customer-mix shifts will all matter for whether Nvidia can keep margins around 75%.

Capital returns remained a bright spot. Nvidia's board authorized an additional $80 billion in share repurchases and raised the quarterly dividend sharply from $0.01 per share to $0.25 per share. That reflects the company's strong cash flow and profitability, while also showing management's willingness to support shareholder returns even at elevated stock levels.

After the report, Nvidia shares fell 1.3% in after-hours trading.

Earnings Call: Jensen Huang Defends the AI Growth Curve

On the earnings call, Jensen Huang argued that mainstream AI has evolved since ChatGPT from one-shot inference to reasoning, and now into the agentic AI phase. In his view, AI is no longer optional; it has become necessary. Tokens are now profitable, and in the AI era, compute capacity is revenue and profit.

Huang said he remains confident in the forecast that Blackwell and Rubin chips can generate $1 trillion in revenue from 2025 to 2027. Management also cited analyst forecasts that hyperscale data center capital expenditure will exceed $1 trillion in 2027, while annual AI infrastructure spending could reach $3 trillion to $4 trillion by the end of 2030.

Huang also pushed back against concerns that Nvidia's inference market share could be eroded by custom chips such as ASICs and LPX. As frontier model companies such as Anthropic join the Nvidia ecosystem, Nvidia's inference compute deployment is expanding sharply. Huang said custom chips have lower throughput and weaker context-processing capability, and will remain a niche product for some time.

Next-generation products were another major focus. Vera Rubin is expected to begin volume shipments in the second half of 2026. Its inference throughput could reach up to 35 times that of Blackwell, and Nvidia expects the product to remain supply-constrained throughout its lifecycle.

Agentic AI also creates a new CPU opportunity. Because agentic AI requires tool use, browser access and orchestration, Huang said GPUs alone are no longer enough and that the market needs a new CPU architecture. He said Vera CPU opens a new $200 billion market that Nvidia has never previously entered. Vera will be sold not only as a companion to Rubin GPUs, but also as a standalone CPU, storage node and security node.

Huang added that Nvidia could see nearly $20 billion of standalone CPU revenue this year, marking the company's ambition to become a leading global CPU supplier.

New Disclosure Framework Could Trigger Repricing

Nvidia also disclosed that it is moving to a new reporting framework designed to better reflect its current and future growth drivers.

The company will establish two major market platforms: Data Center and Edge Computing. Within Data Center, Nvidia will disclose two segments: Hyperscale and ACIE, which includes AI cloud, industrial applications and enterprise applications.

The Hyperscale segment will include revenue from public cloud service providers and the world's leading consumer internet companies. The ACIE segment is intended to show Nvidia's growth opportunity across industries and geographies in AI-purpose-built data centers and AI factories.

The Edge Computing platform will focus on data-processing devices that support agentic AI and physical AI, including PCs, game consoles, workstations, AI-RAN base stations, robotics devices and automotive systems.

This reporting change matters because it could reshape how investors value Nvidia. Instead of viewing the company only through GPU product cycles, the market may increasingly frame Nvidia as a broader AI infrastructure platform spanning hyperscale data centers, enterprise AI, edge devices, CPUs, networking, robotics and physical AI.