Axios said OpenAI is working on a confidential IPO prospectus that could be filed shortly, while timing remains fluid. Capital Brief summarized separate FT, WSJ and Bloomberg reporting that put the most aggressive draft-prospectus window as early as Friday U.S. time, with a possible September debut and a target valuation above $1 trillion. OpenAI's public response was narrower, saying it regularly evaluates strategic options and remains focused on execution.

The market issue is larger than the calendar. A listing would move OpenAI from private capital rounds into a public valuation process just as AI infrastructure demand, data-center financing and custom-silicon alternatives are being priced across Microsoft, Nvidia, Amazon, Oracle, CoreWeave, Broadcom, Goldman Sachs and Morgan Stanley.

Reported Timing Is The Catalyst, Not The Anchor

The strongest version of the current report says a confidential draft could arrive as soon as Friday U.S. time, but Capital Brief also noted Bloomberg's more cautious coming-weeks language. The difference affects liquidity timing because a confidential filing would start the public-offering process without giving the market a full S-1 immediately.

The timing still has force because the IPO calendar is already being pulled forward. Axios said SpaceX disclosed its IPO filing on May 20 and is expected to begin trading in late June under ticker SPCX. OpenAI does not need to list next week for the story to matter. The reported filing window tells public buyers that the private AI leaders may ask the market to absorb unusually large new equity supply before year-end.

The Valuation Gap Starts Above An $852 Billion Base

OpenAI said on March 31 that it closed a funding round with $122 billion in committed capital at an $852 billion post-money valuation. A reported IPO valuation above $1 trillion would not be a fresh startup premium from a low base. It would ask public markets to ratify one of the largest private valuations ever, then pay a higher mark for faster liquidity and disclosure.

The operating case has scale behind it, but the numbers still need the discipline of a prospectus. OpenAI said it was generating $2 billion in revenue per month, that enterprise made up more than 40% of revenue, and that enterprise could reach parity with consumer revenue by the end of 2026. Those are large company-reported markers. A public filing would need to show gross margin, losses, compute commitments, revenue concentration and partner economics in a form the private round did not have to disclose.

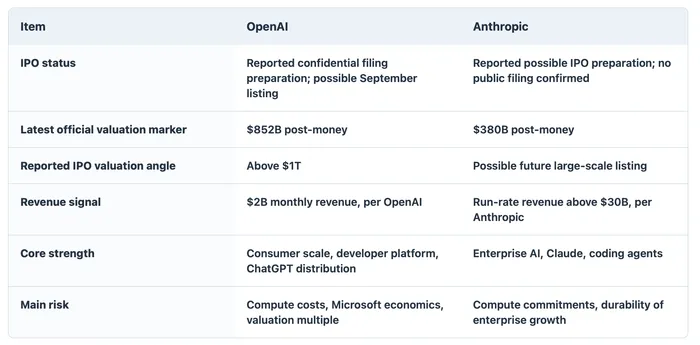

Anthropic Turns OpenAI's IPO Into A Relative-Value Test

OpenAI's reported IPO push should not be viewed in isolation. Reuters, citing the Financial Times, reported in December that Anthropic had hired Wilson Sonsini to prepare for a possible IPO as early as 2026, while Anthropic said it had not decided when or whether to go public. That makes OpenAI's valuation story a relative-value comparison rather than a single-company event. The public market may soon compare OpenAI's consumer-scale platform, developer ecosystem and infrastructure flywheel with Anthropic's enterprise-heavy Claude franchise and coding-agent demand.

The contrast starts with revenue labels that are not fully comparable. OpenAI said it was generating $2 billion in monthly revenue and had raised $122 billion at an $852 billion post-money valuation. Anthropic said in February that it raised $30 billion in Series G funding at a $380 billion post-money valuation and had reached $14 billion of run-rate revenue. Its April Google and Broadcom announcement said run-rate revenue had surpassed $30 billion, up from about $9 billion at the end of 2025. The table below treats those figures as disclosure markers, not a mechanical multiple calculation.

Disclosure note, OpenAI and Anthropic use different revenue disclosure routes, dates and accounting treatment; the table compares current markers and should not be used for mechanical valuation multiples. Sources include OpenAI, Capital Brief, Anthropic's February funding release, Anthropic's April compute announcement and Reuters via Investing.com.

Compute prevents Anthropic from being an easy counterweight. Investing.com summarized Wall Street Journal figures saying Anthropic was projected to lift revenue from $4.8 billion in the first quarter to $10.9 billion in the second quarter and post $559 million of operating profit, with model training costs included and stock-based compensation excluded. Axios reported Anthropic is paying SpaceX $1.25 billion per month through May 2029 for compute capacity. The comparison sharpens OpenAI's IPO burden because public buyers will not only ask whether frontier AI revenue grows. They will ask whether compute obligations fall fast enough for that revenue to carry software-like margins.

Listing order can set the next private-market anchor. If OpenAI lists first above $1 trillion, it could lift private AI marks and keep Nvidia, cloud providers and data-center operators tied to larger capacity plans. If Anthropic's enterprise momentum looks easier to model, OpenAI's premium will need more than ChatGPT reach. It will need prospectus evidence that consumer scale, developer adoption and partner economics can justify a premium to the rest of the AI lab universe.

Public Proxies Split Across Compute, Cloud And Fees

Because OpenAI is not yet public, the listed-market read-through runs through role-specific assets. OpenAI saidNvidia remains the foundation of its infrastructure, with its training fleet and the majority of its inference stack still running on Nvidia GPUs. That gives NVDA the clearest hardware revenue link, but it also raises the margin question if public markets focus on how much compute OpenAI must keep buying to sustain growth.

Microsoft, Amazon, Oracle, CoreWeave and Google Cloud sit on the cloud-capacity side, while AMD, AWS Trainium, Cerebras and Broadcom-linked in-house silicon define the second-source and custom-chip path. Goldman Sachs and Morgan Stanley have the banking-fee angle because the same report says they are leading the raising. Those roles should not be treated as one AI basket. Compute suppliers get paid through capacity demand, cloud partners through usage and commitments, and underwriters only if the listing advances.

Compute Access Is The Margin Mechanism

OpenAI's March announcement made compute the center of the business model. The company said durable compute access advances research, improves products, expands access and lowers the cost of delivery at scale. It also said its infrastructure strategy spans cloud through Microsoft, Oracle, AWS, CoreWeave and Google Cloud, silicon through Nvidia, AMD, AWS Trainium, Cerebras and an in-house chip with Broadcom, and data centers through Oracle, SBE and SoftBank.

That breadth gives OpenAI bargaining leverage, but it also creates the central public-market burden. Revenue growth can look extraordinary while cash needs remain extraordinary. The favorable path is that consumer reach, enterprise adoption, developer usage and cheaper delivery turn compute spending into operating leverage. The weaker path is that usage growth requires so much external capacity that public shareholders discount the revenue multiple before profitability is visible.

The Filing Will Have To Expose Losses And Partner Economics

OpenAI has already broadened access to capital. The company said it expanded a revolving credit facility to about $4.7 billion with a bank syndicate that includes JPMorgan Chase, Citi, Goldman Sachs, Morgan Stanley and other lenders. That financing line supports flexibility, but it also points to the public filing items that will matter most.

The next useful evidence is not another report about the filing date. It is the prospectus detail around revenue durability, gross margin, net loss, capital commitments, Microsoft economics, Nvidia dependence, custom-chip substitution and cloud capacity terms. If those disclosures show compute costs falling as enterprise revenue scales, the reported $1 trillion target becomes easier to defend. If they show revenue growth tied to rising obligations and limited margin visibility, Anthropic becomes the benchmark rather than a sidebar. The IPO market is not only being asked to value one AI company. It is being asked to decide which frontier-AI model deserves the premium, consumer-scale distribution or enterprise-heavy monetization with a clearer productivity story.