Oracle Corporation (ORCL) delivered what would normally be viewed as a strong quarter . Revenue, earnings, margins, backlog, and remaining performance obligations all exceeded expectations, reinforcing the narrative that Oracle has become one of the biggest beneficiaries of the artificial intelligence infrastructure boom. Yet shares fell roughly 6% following the report as investors focused less on what Oracle achieved in fiscal fourth quarter results and more on what it will cost to sustain that growth.

The reaction highlights the central debate surrounding Oracle today. The company is no longer being judged solely on cloud growth or earnings beats. Instead, Oracle has become the poster child for the broader AI financing discussion: How much capital can hyperscalers spend before investors begin demanding proof of returns?

On the surface, the quarter was impressive. Oracle reported adjusted earnings per share of $2.11, easily ahead of the $1.96 consensus estimate. Revenue climbed 21% to $19.2 billion, topping expectations of approximately $19.1 billion. Cloud revenue surged 47% to $9.9 billion, while Oracle Cloud Infrastructure (OCI) revenue jumped 93% to $5.8 billion, essentially matching the lofty expectations analysts had entering the release.

However, the real headline was not revenue or earnings.

It was backlog.

Oracle reported remaining performance obligations (RPO) of $638 billion, an increase of $85 billion sequentially and a staggering 363% year-over-year gain. Wall Street had been expecting roughly $590 billion. The figure represents one of the largest backlog increases ever reported by a major technology company.

Management disclosed that Oracle signed $67 billion of AI infrastructure contracts during the quarter alone. Many of those deals were structured with customer prepayments or bring-your-own-hardware arrangements, helping reduce Oracle's funding burden while simultaneously providing greater visibility into future revenue streams.

The size of the backlog provides investors with extraordinary visibility. According to management, approximately 12% of RPO is expected to be recognized over the next twelve months, while another 34% will be realized between years one and three.

For bulls, that visibility is difficult to ignore.

Scotiabank described Oracle as being at the "center of gravity" for AI infrastructure and maintained its Sector Outperform rating despite reducing its price target from $290 to $241. Citi maintained its Buy rating and $330 target, arguing that the company's growing use of customer prepayments and bring-your-own-hardware structures is helping reduce financing intensity while supporting long-term growth.

Yet even those bullish analysts acknowledge that funding remains the primary issue.

Oracle's free cash flow profile continues to generate concerns. While free cash flow came in better than feared at negative $1.3 billion during the quarter, the company is embarking on one of the most aggressive capital spending programs in corporate history.

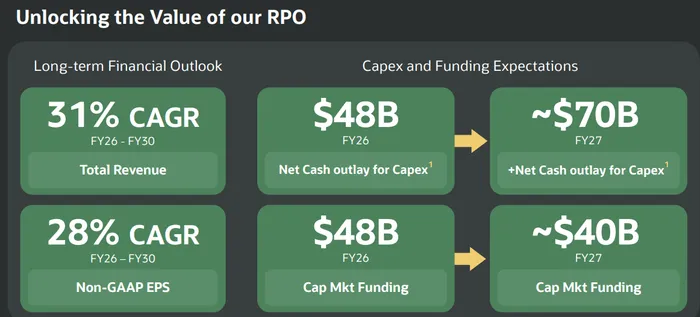

Oracle guided fiscal 2027 capital expenditures to between $90 billion and $95 billion.

That number immediately grabbed Wall Street's attention.

Using management's midpoint guidance of $92.5 billion and Oracle's reaffirmed fiscal 2027 revenue target of $90 billion, Oracle's capex-to-revenue ratio now exceeds 100%.

No major hyperscaler currently operates anywhere near those levels.

Management attempted to soften the concern by noting that approximately $20 billion to $25 billion of the spending will be offset through customer prepayments, reducing net cash outlays to roughly $70 billion. Nevertheless, Oracle still plans to raise approximately $40 billion through a combination of debt and equity financing during fiscal 2027, including a previously announced $20 billion at-the-market stock issuance.

That financing requirement remains the largest overhang on the stock.

Stifel noted that investors were disappointed by management's comments regarding fiscal 2027 profitability as gross margins are expected to decline materially while data center investments ramp. The firm expects gross margins to contract roughly 1,000 basis points year-over-year, significantly worse than prior estimates.

Oracle CFO Hilary Maxson confirmed that gross margins will step down in fiscal 2027 due to the massive data center expansion currently underway. While management expects margins to recover as facilities reach full utilization, investors remain cautious about underwriting those future returns.

Adding another layer of complexity is a report from The Wall Street Journal suggesting OpenAI is considering substantial price cuts as competition with Anthropic intensifies.

According to the report, OpenAI is evaluating significant reductions in token pricing as enterprise customers increasingly push back against escalating AI costs. Anthropic has gained considerable momentum recently, particularly with its coding-focused products, forcing OpenAI to become more aggressive on pricing.

That development matters because Oracle has become one of the largest infrastructure beneficiaries of OpenAI's growth.

If AI providers begin competing aggressively on price, investors may begin questioning whether the industry's extraordinary infrastructure spending plans can ultimately generate acceptable returns. The concern is not demand. Demand remains overwhelming. Oracle reported GPU utilization rates approaching 98%, and management repeatedly emphasized that customer demand still far exceeds available supply.

Instead, the concern revolves around economics.

If OpenAI and Anthropic enter a pricing war while hyperscalers simultaneously spend hundreds of billions of dollars building capacity, the path to sustainable profitability becomes less clear.

That is why Oracle has become such an important stock for the broader AI trade.

The company sits directly at the intersection of the two competing narratives. Bulls see unprecedented backlog growth, accelerating cloud adoption, robust AI demand, and a business that could generate enormous earnings power once infrastructure investments mature. Bears see rising leverage, declining near-term margins, unprecedented capital intensity, and growing questions about whether AI customers will ultimately generate sufficient returns to justify the spending.

From a technical perspective, shares initially plunged toward the $184 level following the earnings release before stabilizing. That area now represents critical near-term support. While the stock remains well above its spring lows near $145 and continues to hold above key long-term moving averages, investors appear reluctant to aggressively chase shares higher until management demonstrates that the current spending cycle can produce meaningful free cash flow.

Ultimately, Oracle delivered a quarter that largely validated the bullish demand story. Revenue exceeded expectations. Earnings beat estimates. Backlog exploded higher. AI contracts continued to accelerate.

But Wall Street already knew demand was strong.

What investors are trying to determine now is whether the economics of AI infrastructure can justify the enormous capital commitments required to build it.

Until that question is answered, Oracle will likely remain the market's primary battleground stock in the debate over AI financing.