Pakistan's energy picture has flipped from one of oversupply to acute shortage in just a few months. The crisis is rooted in a steady decline in domestic production that had already begun to tighten the supply noose. Over the 2024-25 period, domestic natural gas output fell 4.1%, part of a broader drop in indigenous energy as the country leaned more on imports. This trend of aging fields and limited drilling meant that even as gas reserves grew, actual output did not keep pace, creating a vulnerability that would soon be exposed.

At the start of this year, the situation was the opposite. With demand falling for three consecutive years, Pakistan found itself with more imported liquefied natural gas (LNG) than it could use. The government had to take extraordinary steps to manage the oversupply, quietly selling excess shipments abroad and even shutting down domestic gas wells to prevent pipeline pressure from causing a rupture. The surplus was so pronounced that unused gas was being pushed into household networks at a financial loss, adding to the sector's debt burden.

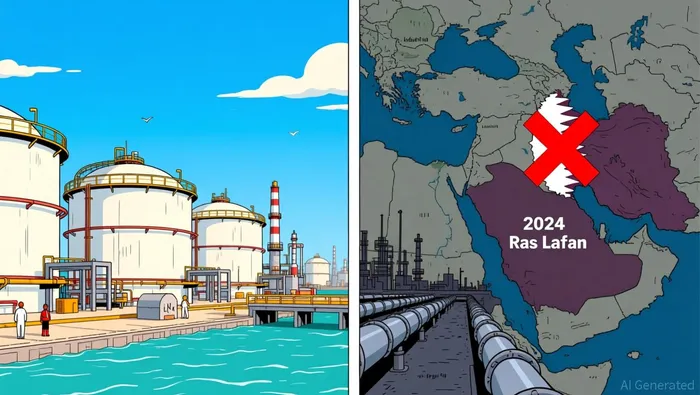

The trigger for this dramatic reversal was the Middle East conflict that erupted in February 2026. The immediate energy consequence was a direct hit to Pakistan's primary supply source. In retaliation for strikes on Iran, Iranian drones hit Qatar's gas facilities at Ras Laffan, the world's largest LNG export complex. In response, Qatar halted all production and declared force majeure, abruptly cutting off Pakistan's nearly exclusive LNG supplier. This action, coupled with the near-halt of traffic through the Strait of Hormuz, severed the main supply route. The result was a sudden and severe energy shortfall, forcing Pakistan to abandon its surplus strategy and now consider costly spot purchases for the first time in over two years.

The Emergency Response and Financial Burden

Pakistan's immediate response to the energy shock has been to scramble for spot LNG, a move that comes with a steep financial price. The state-owned Pakistan LNG Limited (PLL) has issued tenders for two emergency cargoes to be delivered at Port Qasim in Karachi, with one shipment already arriving last month. That first cargo, arranged by TotalEnergies, came at a price of $18.40 per million British thermal units (MMBtu). This marks the first time Pakistan has tapped the spot market for LNG in nearly three years, a stark reversal from its recent surplus.

The cost of this emergency lifeline is now soaring. With spot prices in Asia surging to $20-$30/MMBtu, Pakistan is facing premiums of 25% to 88% over its previous contractual prices of about $16/MMBtu. This price spike is a direct result of the Middle East conflict, which has trapped Qatari LNG in the Persian Gulf and tightened global supply. For a country already grappling with a fragile economy, these spot purchases represent a significant new burden on public finances and consumer costs.

The financial strain is matched by a severe physical shortfall. The energy crisis has caused a daily electricity deficit of about 4,000 megawatts, with roughly 3,000 MW linked to the closure of regasified LNG-powered electricity units. This loss of generation capacity has forced the government to ration power and consider more expensive alternatives. The situation is a direct compression of the supply-demand balance: production has fallen, a key supply route is blocked, and the resulting deficit is now being met with the most expensive fuel available.

Power Sector Context and Summer Demand Pressure

The immediate crisis is a power shortfall, but the underlying structure of Pakistan's electricity mix provides a crucial buffer. LNG currently accounts for about 10% of power generation, a role that has been critical for meeting evening demand peaks and stabilizing the grid. The bulk of supply now comes from local sources, with 74% of electricity generated domestically from solar, coal, nuclear, and hydropower. This shift is the result of years of investment and a surge in rooftop solar, which has sharply reduced daytime grid demand. The government's long-term plan is to build on this foundation, aiming to raise local generation to over 96% by 2034 to minimize future vulnerability to global LNG disruptions.

This domestic pivot is what allows officials to frame the current shock as manageable. Power Minister Awais Leghari has stated that even if LNG were completely disrupted, the impact on industry and agriculture would be minimal. In a worst-case scenario, prolonged cargo stoppages could lead to one to two hours of load shedding during peak summer evenings. This suggests the system has built-in resilience, but it also highlights the specific vulnerability: the 10% of power from LNG is precisely the fuel used to bridge the gap when solar output fades and demand peaks.

The looming summer season introduces a major new pressure. Analysts warn of persistent electricity shortages in the coming months, driven by two factors. First, restricted LNG shipments from the Middle East remain a key constraint. Second, reduced hydrogeneration is expected due to limited water resources. As the country enters summer, electricity demand is expected to rise, with peak consumption anticipated to reach about 24,000 MW. This combination of constrained supply and rising demand creates a clear risk of outages, even if the overall system is not in crisis.

The government's immediate response is to manage this pressure through rationing and demand-side measures. Countrywide load management is being implemented during peak hours to minimize the use of costly fuels. The goal is to conserve fuel and prevent a spike in electricity tariffs. Yet, the path forward remains fraught. While the domestic power base is stronger, the reliance on LNG for peak stability means that any further disruption to the Qatari supply chain could quickly test the system's limits, making the summer months a critical test of Pakistan's energy security.

Catalysts, Structural Risks, and What to Watch

The path out of Pakistan's energy crisis hinges on a single, volatile factor: the resolution of Middle East tensions. The primary catalyst for normalizing supply is the reopening of the Strait of Hormuz to LNG traffic. Until that waterway is secure, the four LNG tankers loaded in Qatar remain trapped in the Persian Gulf, unable to reach Pakistan. This physical blockade is the root cause of the spot market scramble and the daily 4,000-megawatt power deficit. Any diplomatic de-escalation that restores safe passage would allow the backlog of Qatari LNG to flow, potentially easing the immediate pressure on spot prices and the power grid.

Yet the crisis exposes a deeper, long-term imbalance. Pakistan's energy strategy is built on a shrinking domestic base and a single, vulnerable import source. The country's domestic natural gas output has been in steady decline, falling 4.1% over the 2024-25 period. This trend is set to continue even as global demand for LNG grows. Projections point to a significant expansion in the global LNG market, with demand expected to reach 18.4 million tonnes per year by 2050. For Pakistan, this means a structural risk: its own production is falling while its reliance on a contested, concentrated supply chain is likely to increase. The recent conflict has already shown how a single attack can halt production at the world's largest export complex, a vulnerability that will persist without a major diversification of suppliers.

The immediate financial risk is a burden that compounds an already crippling situation. The government's move to buy spot LNG at $22-$25/MMBtu-a premium of 25% to 88% over its previous $16/MMBtu contractual price-directly adds to the energy sector's debt pile. This is the same financial strain that existed when Pakistan was forced to push gas into households at a loss during its surplus phase. Now, the cost of emergency fuel is pushing that debt higher. Analysts note that while spot purchases are a necessary short-term lifeline, they come at a steep price for the economy. The government's choice is stark: pay a premium for LNG to avoid even more expensive fuel oil, or risk deeper, more widespread outages.

What to watch, then, is a race between diplomacy and physical constraints. The reopening of the Strait is the essential first step. But even if that happens, the country must manage the financial fallout of its spot buys while addressing the structural flaw of its energy mix. The summer months will be a critical test, as rising demand meets a supply chain still recovering from a major shock.