Palantir Technologies (PLTR) remains one of the most hotly debated names in the market, with the divide centering less on execution and more on valuation. The company is delivering some of the fastest growth and strongest margins in software, powered by surging demand for its AI platform, yet the stock continues to face skepticism given its premium multiple near 100x forward earnings. Bulls argue that Palantir is emerging as a foundational layer in enterprise and government AI, justifying its elevated valuation, while skeptics question how long such hypergrowth can persist as the company scales. The latest earnings report only intensifies that tension, showcasing exceptional performance while raising the bar even further for what investors expect next.

From a pure numbers standpoint, the quarter was exceptional Palantir reported Q1 revenue of $1.633 billion, up 85% year-over-year, significantly outpacing most large-cap technology peers. Earnings also came in strong, with GAAP EPS of $0.34 and adjusted EPS of $0.33, both ahead of expectations by a wide margin. The company also delivered a roughly 6% revenue beat and nearly 20% upside on EPS relative to consensus, reinforcing its streak of consistent outperformance.

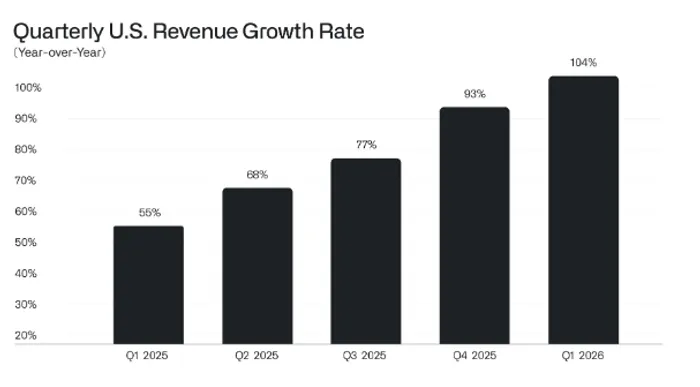

Segment performance was particularly impressive, especially in the United States. U.S. revenue surged 104% year-over-year to $1.282 billion, now representing the majority of the company’s business. Within that, U.S. commercial revenue grew 133% to $595 million, while U.S. government revenue rose 84% to $687 million. This divergence highlights a key theme: Palantir is rapidly expanding its enterprise footprint while maintaining strong momentum in its core government segment.

Commercial and government segments globally also showed strength. Total commercial revenue reached $774 million, while government revenue came in at $858 million. The company continues to benefit from both enterprise AI adoption and geopolitical tailwinds, particularly as defense and intelligence agencies increase spending on data-driven platforms.

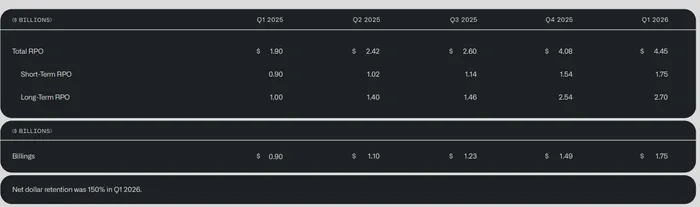

Growth was supported by strong deal activity and backlog expansion. Palantir closed 206 deals worth at least $1 million, including 47 deals over $10 million. Total contract value reached $2.41 billion, up 61% year-over-year, while remaining deal value and backlog metrics also expanded meaningfully. These figures suggest that demand remains robust and that future revenue visibility is improving.

Margins were arguably the most impressive part of the report. Adjusted operating margin reached 60%, while GAAP operating margin came in at 46%. Net income totaled $871 million, representing a 53% margin, and adjusted free cash flow reached $925 million, or 57% margin. These levels are rare even among top-tier software companies and place Palantir closer to the profitability profile of leading semiconductor firms.

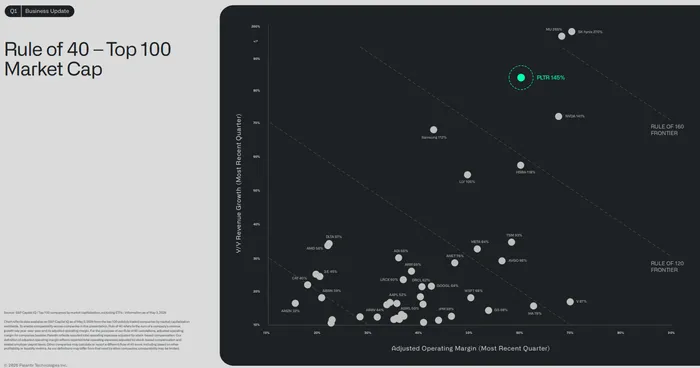

That profitability is captured in the company’s Rule of 40 score, which reached an extraordinary 145%. For context, the Rule of 40 is a key metric used by investors to evaluate software companies, combining revenue growth and profitability. A score above 40 is considered strong; Palantir’s score more than triples that threshold, signaling a rare combination of hypergrowth and high margins. This is a key pillar of the bull case, as it suggests the company can grow rapidly without sacrificing profitability.

Guidance was another highlight. Palantir raised its full-year 2026 revenue outlook to between $7.650 billion and $7.662 billion, implying approximately 71% growth—an increase of about 10 percentage points from prior guidance. The company also raised its U.S. commercial revenue guidance to more than $3.224 billion, representing at least 120% growth. Adjusted operating income is expected to reach $4.44 billion to $4.45 billion, while free cash flow is projected at $4.2 billion to $4.4 billion.

For the second quarter, Palantir expects revenue of $1.797 billion to $1.801 billion and adjusted operating income of $1.063 billion to $1.067 billion. These figures point to continued strong growth, though investors will be watching closely for any signs of deceleration as the company scales.

Despite these results, the stock reaction has been muted, reflecting ongoing valuation concerns. At roughly 100x forward earnings, Palantir is priced for sustained hypergrowth, leaving little room for disappointment. Even with its exceptional Rule of 40 score, investors are questioning whether such growth rates can be maintained over time, particularly as the company becomes larger.

There are also structural questions around the business. Palantir remains heavily reliant on U.S. government contracts, which account for a significant portion of revenue. While these contracts provide stability, they also introduce risk tied to budget cycles and political dynamics. International growth, particularly in Europe, has lagged, raising questions about the company’s global scalability.

At the same time, Palantir’s product positioning remains both a strength and a potential limitation. Its ontology-driven platform and AI capabilities are highly differentiated, but also complex and costly to implement, which may limit adoption among smaller enterprises. The company’s reliance on forward-deployed engineers and custom deployments further reinforces its positioning as a high-end, mission-critical solution rather than a mass-market product.

From a technical perspective, the stock is approaching a key inflection point. The $140 level has emerged as critical support, with a potential “gamma flip” zone around that area. A break below $140 could trigger increased selling pressure as options positioning shifts, while holding that level could set the stage for a rebound. Given the stock’s volatility and heavy options activity, these technical levels are likely to play a significant role in near-term price action.

Ultimately, Palantir’s Q1 results reinforce its status as one of the fastest-growing and most profitable companies in the AI ecosystem. The combination of 85% revenue growth, 60% operating margins, and a 145% Rule of 40 score is difficult to ignore. But in a market where expectations are already sky-high, the bar continues to rise.

For investors, the takeaway is clear: Palantir is executing at an elite level—but the stock may need even more to justify its valuation.