Qualcomm (QCOM) heads into earnings with a strange setup: analog semiconductor sentiment has improved after strong reports from Taiwan Semiconductor Manufacturing (TSM), NXP Semiconductors (NXPI), and Texas Instruments (TXN), but Qualcomm remains caught between that broader chip rally and company-specific pressure from handset memory shortages. The stock has rallied roughly 30% over the past three weeks, suggesting some optimism is already priced in, yet shares remain down about 10% year-to-date, meaning the market still has not treated Qualcomm like the cleaner AI or semiconductor winners.

Analyst expectations are not especially aggressive, but that is because the company already warned investors about a softer Q2. Qualcomm previously guided fiscal Q2 revenue to $10.2 billion to $11.0 billion and non-GAAP EPS of $2.45 to $2.65, both below prior Street expectations of roughly $11.12 billion and $2.89, respectively. Current analyst estimates appear clustered around EPS of $2.55–$2.58, implying about a 10% year-over-year decline, with revenue expected to fall low-single-digits year-over-year.

QCOM Q1 Slide:

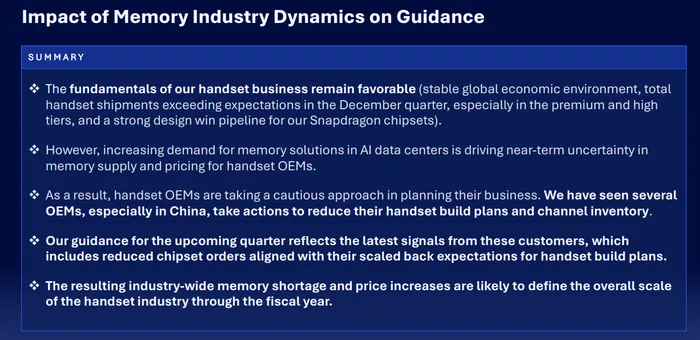

The key issue is the handset business. Qualcomm’s prior quarter was strong, with record total revenue of $12.3 billion and non-GAAP EPS of $3.50, but management said the coming-quarter weakness was entirely tied to memory availability and pricing. CEO Cristiano Amon said handset demand, especially in premium and high-tier devices, was healthy, but DRAM availability for consumer electronics has become constrained as memory suppliers prioritize HBM for AI data centers. In blunt terms, AI is eating the memory supply chain, and handsets are being asked to pick up the check.

By segment, the main unit to watch is QCT, or Qualcomm CDMA Technologies, which includes handsets, automotive, IoT, and related chip businesses. For Q2, management guided QCT revenue to $8.8 billion to $9.4 billion, with QCT handset revenue expected around $6 billion and QCT EBT margins of 26% to 28%. That compares with Q1 QCT revenue of $10.6 billion, including handset revenue of $7.8 billion, IoT revenue of $1.7 billion, and automotive revenue of $1.1 billion. The handset step-down is the core swing factor.

The second major unit is QTL, Qualcomm’s licensing business, which remains very profitable but is expected to decline sequentially. Management guided QTL revenue to $1.2 billion to $1.4 billion, with EBT margins of 68% to 72%, compared with Q1 QTL revenue of $1.6 billion and a 77% EBT margin. That makes QTL less of the headline risk, but it is still important because any weakness in licensing can magnify concerns around the broader handset cycle.

The biggest metric to watch will be handset revenue versus the roughly $6 billion guide. If Qualcomm simply lands in line and says memory pressure is temporary, the stock could hold up given the recent semiconductor rally. If handset revenue misses or Q3 guidance suggests the memory issue is worsening, the market may question whether this is really just a supply-chain issue or the start of a broader demand and share problem.

Automotive is the bright spot. Management expects QCT automotive revenue growth to accelerate to more than 35% in Q2, helped by design wins and longer-term platform adoption. IoT is also expected to grow low-teens year-over-year. These businesses are important to the diversification story, but they are not yet large enough to fully offset handset pressure. That is the whole Qualcomm debate in one sentence: the side businesses are getting better, but the core business is still the landlord.

There are also several notable overhangs. JPMorgan, Bernstein, Seaport, Bank of America, and Morgan Stanley have all flagged versions of the same concern: rising memory prices may pressure smartphone volumes, especially in Android, while Apple’s internal modem roadmap remains a long-term risk. Some analysts expect handset volumes could fall meaningfully if phones become more expensive or OEMs reduce memory content, which could weigh on Qualcomm’s chip sales and royalties.

The OpenAI-related smartphone chip headlines add upside optionality, but investors should be careful not to over-credit them in the near-term model. Reports suggest OpenAI may work with Qualcomm and MediaTek on smartphone processors for a future AI device, but mass production is reportedly not expected until 2028. That may support the “edge AI” story, but it will not fix a Q2 handset shortfall next week. Wall Street is sentimental, but not that sentimental.

For the print, the key items to follow are QCT handset revenue, Q3 guidance, commentary on memory availability, China smartphone demand, Samsung share, Apple modem exposure, automotive growth, and any new details on data center or edge AI initiatives. The market will also listen for whether management repeats that weakness is “100% related to memory,” or whether the language broadens to include demand softness or customer inventory reductions.

Overall, Qualcomm’s setup is mixed. The broader semiconductor tape has improved, peers have posted strong numbers, and the stock still trades at a discount to many chip names. But the 30% pre-earnings rally raises the bar, and the company needs to show that memory shortages are a temporary air pocket rather than a multi-quarter drag on handsets. A clean report with stable Q3 guidance could extend the rebound, but any hint of deeper handset weakness may remind investors why Qualcomm had been out of favor in the first place.