Quantinuum is trying to turn quantum computing scarcity into a public-market number. The Honeywell-backed company is targeting a valuation of up to $12.7 billion in its U.S. IPO, after filing to sell about 21.05 million Class A shares at $45 to $50 each under the planned ticker QNT.

The shock number is the multiple. The target valuation equals roughly 411 times Quantinuum's $30.9 million of 2025 net revenue and about 160 times its $79.3 million of 2025 bookings. The same filing shows a $192.6 million 2025 net loss, so the IPO is asking buyers to pay for a technical lead and a commercialization window before the revenue base has caught up.

Stitched sources include Reuters via MarketScreener and Quantinuum's S-1/A. Symbols are QNT and HON. Date range covers 2025 financials and May 26, 2026 IPO terms. Interval is fiscal year and filing date. Basis is Reuters valuation target, SEC-reported operating metrics and AInvest calculations.

Future Scale Carries Almost The Whole Price

Reuters reported that Quantinuum could raise up to $1.05 billion and that the company raised funds at a $10 billion valuation in September. Moving from that private mark to a $12.7 billion IPO target is less striking than the ratio behind it. A 411 times revenue multiple means almost the entire value sits in future scale, not in the 2025 income statement.

Bookings soften the picture but do not remove the burden. The filing says bookings were $79.3 million for 2025and only $1.3 million for the March 2026 quarter, down from $1.9 million a year earlier. Even the bookings multiple is around 160 times. That keeps the listing from being a conventional growth-stock debate and makes contract flow, revenue recognition and cash use the first public checkpoints.

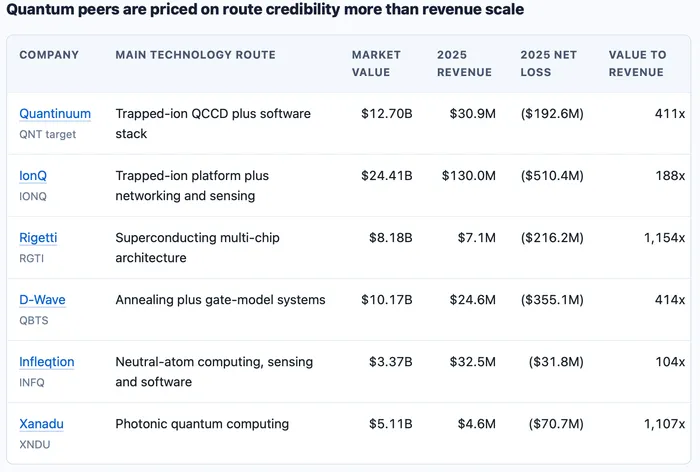

Public Quantum Peers Show The Sector Is Expensive, Not Uniform

Quantinuum is not alone in carrying a valuation far ahead of current revenue. StockAnalysis market-cap snapshots show IonQ at $24.41 billion as of May 27, D-Wave at $10.17 billion, Rigetti near $8.18 billion, Xanadu at $5.11 billionand Infleqtion at $3.37 billion. The peer set says public markets are already paying venture-style prices for several quantum routes, but the revenue bases and technical claims are very different.

Market values use StockAnalysis snapshots checked May 27, 2026, except Quantinuum's proposed valuation from Reuters via MarketScreener. Revenue and loss figures use company filings or releases from Quantinuum, IonQ, Rigetti, D-Wave, Infleqtion and Xanadu. Multiples are AInvest calculations using market value or target valuation divided by 2025 revenue.

The table changes the valuation read. Quantinuum's 411 times revenue target is not obviously outside the public quantum range because Rigetti and Xanadu screen higher on the same simple metric, while D-Wave is in the same zone. It is still far above IonQ's roughly 188 times revenue and Infleqtion's roughly 104 times revenue. That makes Quantinuum expensive, but not isolated. Its relative case depends on whether trapped-ion fidelity, software depth and customer validation deserve a premium over smaller public peers with different hardware paths.

The Positive Case Needs To Rest On Fidelity And Platform Depth

Quantinuum's strongest argument is technical rather than financial. The S-1/A says Helios is a 98-qubit trapped-ion quantum computer, and says its 99.921% two-qubit gate fidelity as of December 31, 2025 was the highest among commercially available gate-based quantum systems based on the cited Ransford study and the company's analysis of peer filings. The filing also describes a trapped-ion, multi-zone QCCD architecture, real-time control electronics and a software stack that includes TKET and Guppy.

That is the moat claim the valuation is really asking the market to underwrite. A high-fidelity trapped-ion system can support the idea that Quantinuum is closer to useful fault-tolerant quantum computing than some alternatives, while the software layer gives customers a way to build workflows across system generations. The company also says it has delivered three successive platforms and is executing a roadmap toward its Apollo system before the end of the decade. Those statements are company claims, not durable economics by themselves, but they explain why the market may pay for more than 2025 revenue.

Customer Validation Is Still Concentrated

The same filing that supports the technology story also shows how early commercial scale remains. Quantinuum says RIKEN accounted for 60% of 2025 revenue and 7% of revenue in the March 2026 quarter, while another government-affiliated research institution accounted for 47% of March-quarter revenue. The U.S. government accounted for 24% of March-quarter revenue and 16% of 2025 revenue.

Those figures do not cancel the platform claim. They do make early public quarters sensitive to contract timing, grant milestones and research-institution demand. Revenue fell to $5.2 million in the March 2026 quarter from $19.1 million a year earlier, while the quarterly net loss widened to $136.6 million from $30.5 million.

Honeywell And Federal Funding Add Support With Strings Attached

Honeywell remains the anchor asset behind the listing. Quantinuum said in the filing that Honeywell entities will beneficially own about 49.1% of the combined voting power after the offering, or about 48.5% if the underwriters fully exercise their option. For HON, the IPO creates a public mark for a business it still largely influences, and QNT's first disclosures may feed back into how the market values Honeywell's technology portfolio.

Federal support adds a policy floor but not a commercial guarantee. The Commerce Department announced letters of intent for $2.013 billion in CHIPS Act quantum incentives across nine companies, including $100 million in planned funding for Quantinuum. The department also said it will receive a minority, non-controlling equity stake in each company as a funding condition.

The Public Market Hurdle Is Now Specific

The next hurdle is not whether quantum has policy and investor attention. Public markets already show they will pay high multiples for IonQ, Rigetti, D-Wave, Infleqtion and Xanadu. Quantinuum's issue is whether its 411 times revenue target is backed by a technical lead that can survive comparison and by customer demand that can broaden beyond a few large relationships.

Final IPO pricing, first trading close, post-offering ownership, bookings, revenue recognition, customer concentration, cash burn and Helios-to-Apollo technical milestones now carry the argument. If those disclosures improve, the premium can look like a scarcity price on a leading platform. If bookings stay lumpy or peer multiples compress, the same 411 times revenue math will make the valuation look less like a technology premium and more like a funding round moved onto Nasdaq.