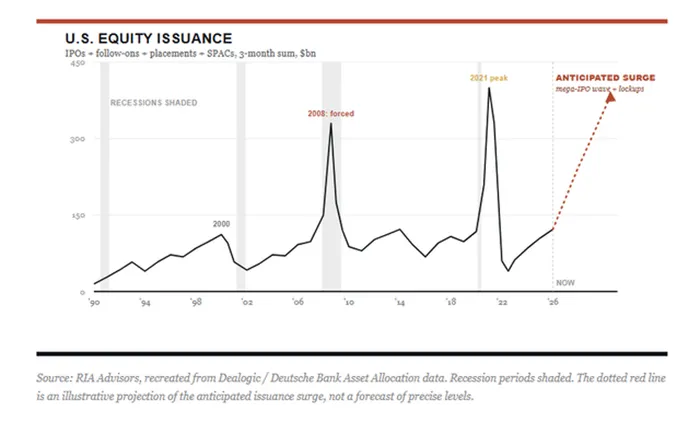

For most of the last two decades, one of the most powerful yet underappreciated forces supporting U.S. equities had nothing to do with earnings, interest rates, or economic growth.

It was supply.

More specifically, the lack of it.

According to recent Financial Times reporting citing Goldman Sachs data, net U.S. equity supply is expected to be essentially flat in 2026 after shrinking every year since 2003. That may not sound particularly dramatic, but it represents a major shift in one of the market's most important structural tailwinds.

For years, corporations have been removing shares from the market through stock buybacks, mergers, acquisitions, and privatizations. Investors consistently had fewer shares to buy while capital flowing into equities continued to increase. That imbalance helped support valuations and amplified market rallies.

Now the dynamic is changing.

A massive wave of equity issuance is beginning to emerge just as central banks are tightening policy, Treasury borrowing is accelerating, and investors are already wrestling with elevated valuations across technology and artificial intelligence.

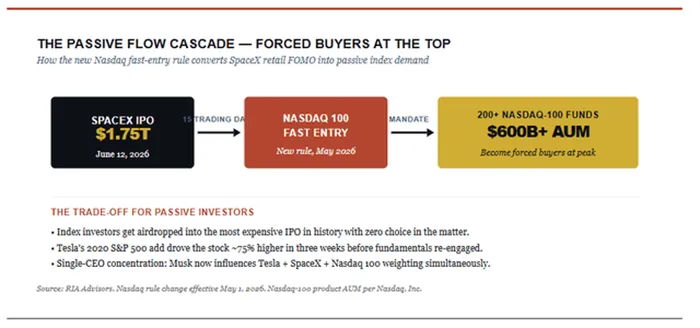

The poster child for this shift is SpaceX.

The company is expected to price its IPO this week at $135 per share, raising roughly $75 billion and commanding a valuation approaching $1.75 trillion. Even before the company begins trading, institutional demand has reportedly surpassed $250 billion, making the deal nearly four times oversubscribed.

On the surface, strong demand appears bullish.

However, market mechanics tell a more complicated story.

Every dollar allocated to SpaceX is a dollar that cannot simultaneously be invested elsewhere. Large institutional investors operate under fixed risk budgets and portfolio constraints. If billions of dollars are allocated to a new IPO, those funds often come from selling existing holdings.

That creates what market strategists sometimes refer to as a "capital vacuum."

The issue becomes even more pronounced when the IPO is concentrated in the technology sector.

SpaceX is not arriving alone.

OpenAI is expected to eventually pursue a public listing. Anthropic remains a likely IPO candidate. Reports suggest SK Hynix may seek a U.S. listing as early as this year. Meanwhile, existing public companies are raising capital at an accelerating pace.

Super Micro Computer Inc. (SMCI) just announced roughly $7 billion in equity and equity-linked financing. Reports suggest Alphabet Inc. (GOOGL) and Meta Platforms, Inc. (META) could explore sizable capital raises to support artificial intelligence initiatives. Oracle Corporation (ORCL) continues to raise debt and pursue alternative financing structures to fund its massive cloud infrastructure expansion.

Collectively, this represents a dramatic increase in equity supply.

The timing is important.

Historically, periods of significant issuance have often coincided with market peaks rather than market bottoms.

One notable example occurred during the technology bubble of the late 1990s. As valuations surged and investor enthusiasm became extreme, companies rushed to issue stock and bring new businesses public. The IPO calendar exploded in 1999 and early 2000 just as the Nasdaq approached its peak.

The reasoning was straightforward.

Management teams and private investors recognized elevated valuations and sought to monetize them.

The same phenomenon occurred during portions of the SPAC boom in 2020 and 2021. Record issuance eventually overwhelmed investor demand, contributing to significant underperformance once market liquidity began tightening.

That does not mean today's environment is identical.

The artificial intelligence investment cycle appears supported by real demand, real revenues, and genuine infrastructure requirements. However, market history demonstrates that supply matters.

Even the strongest investment themes can struggle when too much paper comes to market simultaneously.

The challenge extends beyond equities.

Investors are also confronting a significant increase in competing sources of capital demand.

The European Central Bank is expected to raise rates this week. Markets continue to price another Federal Reserve hike later this year. Treasury auctions remain elevated as the U.S. government finances growing deficits, with fresh 10-year and 30-year bond issuance scheduled this week.

Every one of those developments competes for investor dollars.

Higher interest rates increase the attractiveness of fixed income. Treasury issuance absorbs liquidity. Central bank tightening reduces the amount of capital available to support financial assets.

The result is a market environment where liquidity becomes increasingly important.

SIFMA data illustrates the broader trend. Total U.S. debt issuance continues to rise as governments and corporations finance larger capital requirements. Meanwhile, artificial intelligence infrastructure projects require unprecedented levels of investment.

Oracle, who reports tonight, provides a useful example.

The company sits at the center of the AI funding debate because it is simultaneously one of the industry's largest beneficiaries and one of its largest borrowers. Oracle's remaining performance obligations exceed $500 billion, reflecting enormous future demand for cloud and AI services. Yet fulfilling that demand requires massive capital expenditures and increasingly creative financing arrangements.

The concern is not necessarily whether demand exists.

It is whether capital markets can continue funding the required infrastructure without creating strains elsewhere.

This is where the SpaceX IPO becomes particularly important.

The company is effectively serving as a test case for investor appetite.

Can markets absorb one of the largest IPOs in history while simultaneously funding AI infrastructure, supporting secondary offerings, financing government deficits, and maintaining elevated equity valuations?

So far the answer appears to be yes.

But markets are beginning to show signs of strain.

Technology stocks have struggled recently despite generally favorable earnings trends. Semiconductor names have experienced profit-taking. Volatility has increased. The CBOE 1-Month Implied Correlation Index recently reached extreme levels of bullish positioning before reversing sharply.

These developments may be early indications that investors are becoming more selective.

The Nasdaq's recently adopted fast-entry rule adds another wrinkle. Under the new framework, large companies can enter major indices much more quickly than in the past. If SpaceX gains rapid inclusion in the Nasdaq-100, passive funds could become forced buyers at elevated valuations, creating another layer of demand while simultaneously increasing concentration risks.

The chart below highlights the concern. A company can effectively move from IPO to passive index ownership in a matter of days, forcing hundreds of billions of dollars in benchmarked assets to gain exposure regardless of valuation.

That may create near-term support.

It does not eliminate longer-term risks.

Ultimately, the biggest question facing investors is whether demand can continue growing faster than supply.

For years, shrinking share counts and aggressive buybacks provided a powerful tailwind for equities. That tailwind is fading. In its place is a market that must absorb IPOs, secondary offerings, debt issuance, and massive infrastructure financing requirements all at once.

The AI boom remains intact. Economic growth remains resilient. Corporate earnings continue to expand.

But market mechanics matter.

As 2026 progresses, investors may discover that the biggest challenge facing equities is not demand for artificial intelligence, but rather the growing amount of capital required to fund it.