Samsung Electronics turned AI memory into a labor-risk trade on Friday, May 15, after Reuters reportedthat its South Korean union stayed with a planned strike starting May 21 and shares fell as much as 9.3%. The prior assumption was cleaner: tight HBM and server-memory demand would keep the memory cycle pointed upward. The new risk is whether the same demand can still convert into reliable output and customer commitments if labor disruption reaches chip production.

Friday's reaction was not isolated to one Korean stock. Investing.com reported that Micron fell nearly 5%, Nvidia dropped 3.5%, Broadcom shed 3%, AMD fell 3.7%, Intel dropped 6% and ASML fell 4.5% during the same chip-stock selloff. That does not prove Samsung's strike risk caused every move, because KOSPI pressure and U.S.-Iran headlines were also in the tape. It does show why a labor dispute at a dominant memory supplier can move through the AI hardware chain quickly.

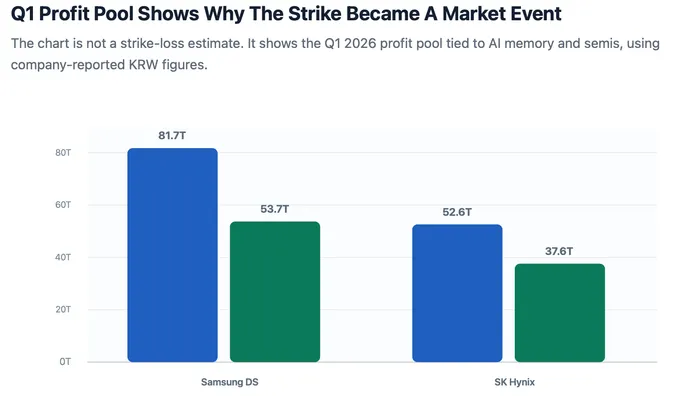

Sources: Samsung Electronics Q1 2026 results and SK Hynix Q1 2026 results. Values are revenue and operating profit in KRW trillions; Samsung is shown as Device Solutions, not a pure memory-only segment.

Labor Risk Hits The Memory Trade Differently

Reuters' stock read gives the catalyst hierarchy. Samsung shares were down 9.3% at 0556 GMT against a 7.0% fall in the KOSPI, while the union said it would keep plans for an 18-day walkout from May 21 and consider talks after June 7. The union also warned that more than 50,000 workers could walk off the job. In that setup, the market is not only reacting to a pay dispute. It is discounting the chance that production reliability becomes a customer-allocation issue.

For Samsung, the pressure is direct. Customers that need HBM, high-density DRAM or advanced memory packaging care less about the labor headline than about shipment timing, yield stability and whether committed capacity arrives when planned. Reuters also cited a JPMorgan estimate that a strike could carry a KRW 21 trillion to KRW 31 trillion operating-profit impact and about KRW 4.5 trillion of sales losses. That figure is an analyst estimate, not company guidance, but it gives scale to the risk the stock was trying to price.

Q1 Profit Shows Why The Dispute Became A Market Event

Official first-quarter releases explain why the labor story landed in the AI trade instead of staying inside Korean industrial relations. Samsung said Q1 consolidated revenue reached KRW 133.9 trillion and operating profit reached KRW 57.2 trillion, with the Device Solutions Division posting KRW 81.7 trillion of revenue and KRW 53.7 trillion of operating profit.

Samsung also said its Memory Business set a quarterly revenue and operating-profit record on high-value AI demand and higher average selling prices. SK Hynix reported Q1 revenue of KRW 52.6 trillion, operating profit of KRW 37.6 trillion and a 72% operating margin under K-IFRS, citing AI demand and high-value memory products. Those releases keep the supportive memory-demand read alive, but they also sharpen the downside condition: a supply interruption matters more when customers are already competing for high-end capacity.

Micron And Nvidia Carry Different Exposures

Micron is the cleaner U.S. memory peer. The company reported fiscal Q2 revenue of $23.86 billion and said memory has become a strategic asset in the AI era. If Samsung disruption proves real, Micron's stock can react through pricing, customer allocation and memory scarcity. If talks avert the strike, that peer premium can fade because the original demand backdrop was already visible.

Nvidia's role is different. The company is not a memory producer in this story; it is the platform leader whose accelerators depend on a reliable HBM and advanced-memory supply chain. That makes Nvidia a second-order exposure: supplier reliability matters, but the stock's own earnings, gross-margin guide and customer demand still carry the main burden. SK Hynix sits on the other side of the same debate as Samsung's rival memory supplier and as the compensation benchmark cited in the Reuters labor report.

Production Reliability Is The Next Market Checkpoint

Three disclosures matter more than another broad AI-demand headline. Negotiations before May 21 would tell investors whether the strike risk can be contained. Participation at Pyeongtaek would show whether the labor action is symbolic or operational. Customer and product language around HBM4, server DRAM and eSSD shipments would show whether the issue has moved from sentiment into allocation, delivery or margin expectations.

A negotiated settlement would likely send the trade back to the familiar memory-cycle variables: AI server demand, average selling prices, capex discipline and customer share. A broad walkout would make the market ask a different question, one that is harder to answer from demand data alone. In that case, Samsung's Q1 profit pool becomes less important than whether the company can protect production continuity while SK Hynix, Micron and Nvidia customers watch the same supply window.