ServiceNow (NOW) heads into its Financial Analyst Day under pressure, with investors looking for clarity after a messy first-quarter report triggered a sharp 14% selloff. The reaction wasn’t about a collapse in fundamentals—far from it—but rather a combination of muddied messaging, concerns around slowing organic growth, and a growing debate over whether artificial intelligence is a tailwind or a threat to the company’s business model. At the heart of the debate is a broader market narrative: “AI eats software.” For ServiceNow, which positions itself as the “AI control tower” for enterprise workflows, the challenge is convincing investors that it will be the beneficiary—not the victim—of that shift.

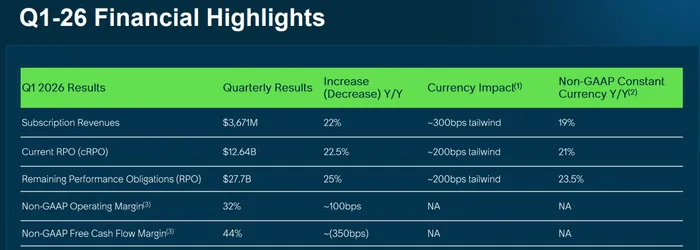

The first-quarter numbers themselves were solid on the surface. ServiceNow reported adjusted EPS of $0.97, in line with expectations, on revenue of $3.77 billion, slightly above the $3.74 billion consensus. Subscription revenue came in at $3.67 billion, growing 19% year-over-year, while current remaining performance obligations (cRPO) reached $12.64 billion, up 22.5%. The company also highlighted a strong 97% renewal rate, reinforcing the stickiness of its platform. By most traditional measures, this was a healthy quarter.

Yet the stock reaction suggested otherwise, falling roughly 13–14% in the aftermath. The issue wasn’t what the company delivered—it was how it delivered it. Investors had been positioned for a clean “beat and raise” quarter, but instead got a mix of modest beats, slightly underwhelming forward guidance, and confusion around organic versus inorganic growth contributions. Several analysts pointed to a deceleration in key metrics, with organic current bookings growth slipping into the single digits at around 9.6% and expected to fall further to roughly 5.4% in the next quarter.

Geopolitics also played a role, though perhaps more in perception than reality. Management cited delayed on-premise deals in the Middle East as a roughly 75-basis-point headwind to subscription revenue, and similar delays weighed on backlog metrics. But while these factors are largely timing-related, they contributed to a narrative that growth is becoming less predictable—something the market has little patience for in the current environment.

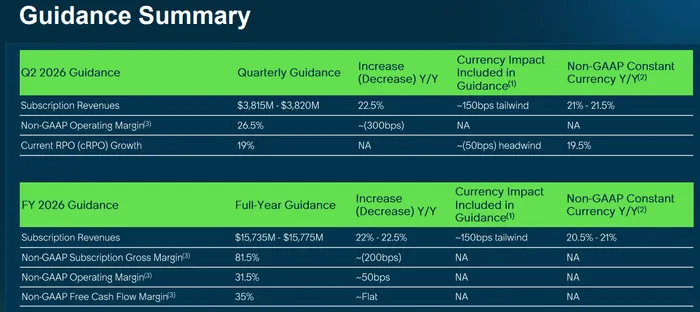

Guidance added to the confusion. ServiceNow guided second-quarter revenue to $3.815 billion to $3.82 billion, below the $3.86 billion consensus, and maintained a relatively conservative full-year outlook of $15.735 billion to $15.775 billion. While management did raise its subscription revenue guidance modestly, the tone was seen as cautious, reinforcing the idea that near-term acceleration is unlikely. Analysts broadly interpreted the guidance as prudent rather than bullish, which in this market often translates to disappointment.

Margins also became a focal point. Subscription gross margins declined by roughly 300 basis points, driven in part by the integration of acquisitions such as Armis. While operating margins held up better—coming in around 32% and exceeding guidance—investors remain concerned that AI-related investments could pressure profitability over time. This concern was amplified by commentary suggesting that AI could reduce seat-based pricing power, a key pillar of the traditional software model.

That brings the discussion back to AI, which remains both the biggest opportunity and the biggest question mark. On the bullish side, ServiceNow is seeing strong traction with its AI offerings, with management raising its AI annual contract value (ACV) target to $1.5 billion for 2026, up from $1 billion previously. The company’s Now Assist product continues to outperform expectations, and management emphasized that AI is embedded across its platform, driving larger deal sizes and deeper customer engagement.

However, skeptics argue that AI may not be as incremental as hoped. Some analysts have pointed out that increased AI capabilities could lead customers to reduce headcount or negotiate lower prices, effectively offsetting the benefits. Others have questioned whether ServiceNow’s AI revenue is truly incremental or simply a repackaging of existing functionality. This uncertainty has made it difficult for investors to fully buy into the AI-driven growth narrative.

The Financial Analyst Day presents an opportunity for management to reset that narrative. Investors will be looking for clearer articulation around how AI drives incremental revenue, how pricing models are evolving, and how the company plans to sustain double-digit growth in a potentially slowing software environment. There is also interest in new pricing tiers—Foundation, Advanced, and Prime—which incorporate AI usage and could signal a shift toward a more consumption-based model.

Analyst sentiment, while mixed, remains broadly constructive. Price targets have come down across the board, reflecting near-term uncertainty, but many firms maintain Buy or Outperform ratings. Bulls argue that the underlying business remains strong, with a large and growing addressable market, high customer retention, and significant opportunities in AI, cybersecurity, and data integration. Bears, on the other hand, point to valuation, decelerating growth, and competitive pressures as reasons for caution.

From a technical perspective, the stock’s recent price action suggests a potential inflection point. The sharp selloff following earnings may have represented a capitulation event, clearing out weak hands and resetting positioning. There is growing discussion around a potential double-bottom formation, which could provide a foundation for a recovery if fundamentals stabilize and sentiment improves.

The key level to watch is $100, which has emerged as both a psychological and technical resistance point. A sustained move above that level would likely signal renewed confidence and could open the door to further upside. Conversely, failure to reclaim $100 could keep the stock range-bound, particularly if broader software sentiment remains weak.

Ultimately, this Financial Analyst Day is less about new numbers and more about narrative control. ServiceNow doesn’t need to prove that its business is working—it already has. What it needs to do is convince investors that its growth is durable, its AI strategy is additive, and its best days are still ahead. If management can deliver that message clearly and convincingly, the recent selloff may prove to be an opportunity rather than a warning.