SiTime's earnings reaction turned a small component category into a larger AI infrastructure debate. SITM closed May 7 at $797.31, up 27.91%, after the precision-timing company reported a quarter that beat expectations and pointed to a sharper June-quarter step-up.

Before the release, a cautious read was that SiTime would ride the semiconductor cycle with some consumer and networking recovery. After the release, investors had to value a more specific idea: synchronization can become a system-level constraint as AI clusters chase higher utilization, lower latency and denser networking.

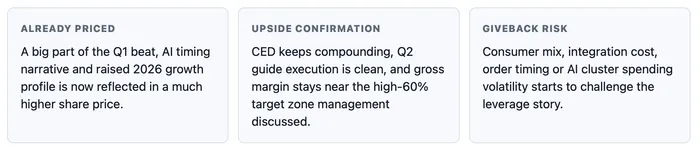

A 28% move prices in a bottleneck story

Price action was the first signal that investors saw more than a routine beat. The stock's May 7 closing movearrived after a Q1 release that showed growth, margins and guidance moving in the same direction, a powerful combination for a small-cap semiconductor name already tied to AI supply-chain scarcity.

Stock moves of that size usually need a cleaner market map. The obvious bullish case is that precision timing is gaining content per AI system. The risk is that the stock begins to capitalize a bottleneck narrative before customers, margins and the Renesas timing acquisition have proved how durable the demand curve really is.

Q1 leverage was stronger than the revenue beat

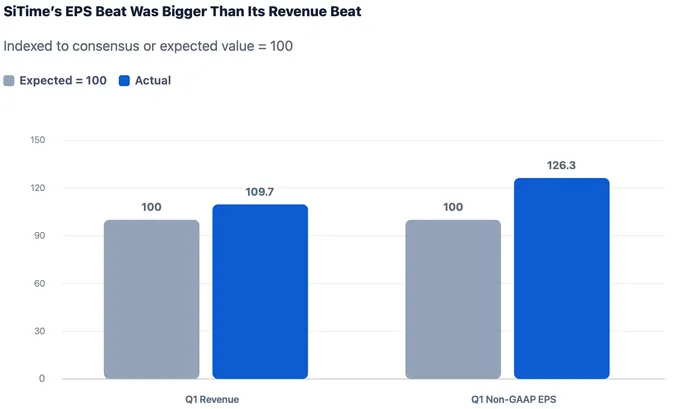

Reported numbers support the re-rating, but they also narrow the burden of proof. Q1 revenue rose 88.3% year over year to $113.6 million, while non-GAAP EPS reached $1.44. The same filing showed non-GAAP gross margin of 64.5% and non-GAAP operating margin of 28.0%.

Consensus context makes the market reaction easier to understand. MarketBeat listed expected revenue of $103.51 million and consensus EPS of $1.14. On that basis, the EPS beat was much larger than the revenue beat, which is exactly the kind of spread investors look for when a hardware supplier argues that mix and pricing power are improving.

Source scope: stitched from SiTime Q1 2026 8-K exhibit for actual revenue and non-GAAP EPS; MarketBeat/Quartr for Q1 expected revenue and consensus EPS.

AI inference moved timing deeper into the stack

SiTime's core argument is that AI infrastructure demand is not just buying accelerators. It is also buying the precision that lets distributed systems run with fewer timing errors. The company says its MEMS timing products are used across AI data centers, automated driving, industrial systems, wearables and other applications, but the latest quarter shifted investor attention toward data-center use cases.

Communications, Enterprise and Data Center revenue reached $75.7 million, or 66.6% of Q1 revenue, and grew 158% year over year. That mix matters because the data-center category is the one most directly tied to AI inference, optical modules, switches, SmartNICs, accelerator platforms and co-packaged optics.

Management also framed inference systems as more timing-intensive than training systems. The MarketBeat/Quartr transcript page said newer XPU-based inference infrastructure needs 2x to 4x more timing content per systemthan training infrastructure. If that relationship holds, SiTime is not merely selling into a broader chip cycle. It is gaining content as the architecture of AI workloads changes.

Precision timing is being sold as a utilization fix

Product context gives the earnings beat a sharper read-through. SiTime's Elite 2 Super-TCXO release says the device delivers sub-nanosecond synchronization across AI clusters and targets a cumulative $1.5 billion market by 2030. Management's message is that timing errors can create wait cycles, data-corruption risk and lower system utilization.

For investors, the market logic is straightforward but still unproven at scale. GPU scarcity and cloud capex have dominated AI infrastructure coverage, while timing and synchronization have looked like lower-profile enabling layers. SiTime's quarter suggests the market may be starting to pay for those layers when they carry high ASPs, high gross margins and direct links to system efficiency.

A stronger bull case would need evidence that Elite 2 and related platforms become repeatable, multi-customer design wins rather than a product-cycle spike. A weaker outcome would show up if utilization claims do not translate into sustained orders or if customers treat precision timing as a temporary catch-up purchase.

Guidance raises the execution bar

Guidance is where the rally becomes harder to defend with Q1 numbers alone. MarketBeat's transcript page showed Q2 revenue guidance of $140 million to $150 million and non-GAAP EPS guidance of $1.85 to $2.00. It also showed the company raising 2026 revenue growth expectations to at least 80%.

Balance-sheet support reduces one source of near-term stress. SiTime ended March with $788.7 million in cash, cash equivalents and short-term investments. That gives the company room to invest, but it does not answer the valuation question after a one-day move that already rewards a lot of future execution.

Renesas timing assets add another layer. The transcript page said the Q2 outlook excludes any benefit from the acquisition because the deal had not closed. That keeps the reported guide cleaner, but it also means investors still have to underwrite integration cost, product overlap, customer retention and eventual margin contribution separately from the organic AI timing story.

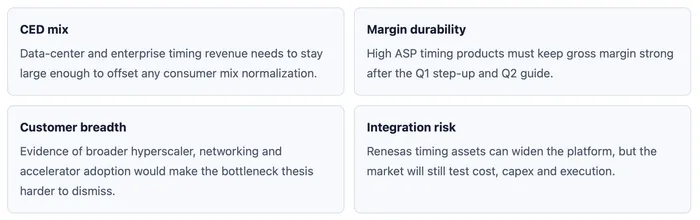

The trade now depends on mix and proof

SiTime has moved into a cleaner watch-list phase. A follow-through rally would be easier to justify if CED remains the dominant growth engine, Q2 revenue lands near or above guidance, non-GAAP gross margin holds around management's target zone, and AI inference demand shows up through multiple customers rather than a narrow order cluster.

The new price says investors are willing to capitalize precision timing as part of the AI infrastructure chain. That is the right debate after this quarter, but expectations are now much higher. SITM's next proof point is whether synchronization demand can keep converting into revenue growth, operating leverage and customer diversity after the first big repricing has already happened.