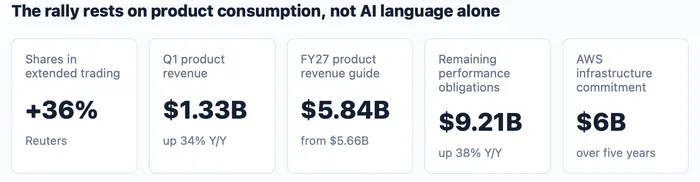

Snowflake turned AI-software skepticism into a consumption-growth rally on May 27. Reuters reported the shares up 36% in extended trading after the company raised its fiscal 2027 product revenue forecast and announced a five-year AWS infrastructure commitment.

Before the report, AI agents had raised concern that software economics could compress faster than vendors could monetize the new usage. Snowflake's report shifts the debate toward companies sitting close to governed enterprise data, where AI usage can show up in product revenue, remaining performance obligations and free cash flow instead of only product demonstrations.

Provider and source are Reuters via Investing.com and Snowflake company releases. This stitched comparison card uses Reuters via Investing.com, Snowflake's Q1 FY27 release and Snowflake's AWS announcement. Product Revenue Carries The Immediate Repricing

Snowflake's strongest evidence is still product consumption. The company reported $1.334 billion of Q1 product revenue, up 34% from a year earlier, and Reuters said total revenue of $1.39 billion topped the LSEG estimate of $1.32 billion.

Management also lifted the full-year FY27 product revenue outlook to $5.84 billion, up from previous guidance of $5.66 billion. That matters because Snowflake's consumption model gives AI demand a clearer revenue channel. More data movement, machine-learning work and agentic application deployment can lift usage without relying only on traditional seat expansion.

Timing remains the counterweight. A raised annual guide can still fade if workload migrations are front-loaded or if first-party AI products do not create incremental usage beyond the core data platform. Near-term disclosure now runs through Q2 product revenue, which Snowflake guided to $1.415 billion to $1.420 billion, above the Reuters-cited LSEG estimate of $1.37 billion.

The AWS Commitment Adds Scale And Dependence

AWS gives the rally a second leg beyond one quarter of revenue. Snowflake said it made a $6 billion multi-year infrastructure commitment to AWS, including Graviton compute and AI spend, and framed the agreement around governed data, generative AI and agentic AI workloads.

That commitment strengthens Snowflake's position inside the AWS ecosystem. The company said lifetime AWS Marketplace sales have surpassed $7 billion and calendar-year 2025 marketplace sales exceeded $2 billion, more than doubling transaction growth from a year earlier. Partnership depth also creates a dependency. Snowflake now needs Graviton performance, Marketplace procurement and joint go-to-market work to help customers scale AI applications without eroding margins.

Margins And Cash Flow Decide Whether Growth Has Quality

Consumption growth is easier to reward when it does not come with weaker economics. Snowflake reported Q1 non-GAAP operating income of $165.8 million, equal to an 11.9% non-GAAP operating margin, and adjusted free cash flow of $265.5 million, equal to a 19.1% adjusted free cash flow margin.

Full-year guidance points in the same direction. Snowflake raised FY27 non-GAAP operating margin guidance to 13.5% from 12.5% and guided to a 23.0% adjusted free cash flow margin. Those numbers keep the stock reaction from being pure revenue-multiple expansion. Operating quality now depends on whether AI-driven usage raises product revenue while product gross margin, operating margin and cash generation improve together.

Software Peers Still Need Different Kinds Of Evidence

Snowflake's move lands in a software tape that was already trying to recover from an AI scare. Reuters wrote on May 19 that U.S. software stocks had been battered by AI disruption fears, while the iShares Expanded Tech-Software Sector ETF was down 12.2% year to date and the S&P 500 software and services index was down 13.7% as of the prior close.

Different revenue mechanisms separate the software names. Reuters reported that BofA analysts treated ServiceNow as harder to challenge because of workflow entrenchment, while Salesforce faced a structural-shift concern. Snowflake's evidence runs through data consumption, customer workloads, RPO and cloud infrastructure alignment rather than per-seat subscription resilience.

Customer Adoption Sets The Follow Through

Snowflake supplied adoption markers that can either support or weaken the next leg. The company said more than 13,600 accounts used Snowflake AI capabilities on its four-week average basis, Snowflake Intelligence accounts more than doubled quarter over quarter and Cortex Code was in use across more than 7,100 accounts.

Adoption markers are not the same as recognized revenue by themselves. Follow-through now depends on whether AI usage keeps translating into product revenue, RPO, operating margin and adjusted free cash flow instead of staying at the product-adoption layer. A stronger Q2 product-revenue print, continued RPO growth and stable margin guidance would support the new read. Slower workload migration, weaker cash conversion or a lower FY27 guide would push the debate back toward software disruption risk.