U.S. equity markets came under heavy pressure Friday as investors finally began confronting a reality that had been building for weeks: rising oil prices, sticky inflation, and surging bond yields are becoming increasingly difficult for equities — especially richly valued AI and technology stocks — to ignore. The S&P 500 fell sharply while the Nasdaq Composite led declines, with semiconductor stocks absorbing the bulk of the damage. But while many investors initially attempted to blame the weaker-than-hoped-for Trump-Xi summit, the larger forces behind the selloff appear to be rooted in bond markets, inflation expectations, and options expiration mechanics.

One of the most important forces impacting markets Friday was options expiration.

Roughly $2.6 trillion in notional options exposure expired , including large amounts of index and single-stock options tied heavily to the AI trade. For weeks, dealer positioning had been characterized by substantial positive gamma exposure, which effectively forced dealers to buy dips and provide liquidity as markets rallied higher. That positioning became one of the key reasons equities repeatedly shrugged off rising Treasury yields and elevated geopolitical uncertainty over the past several weeks. Markets were essentially cushioned by a large amount of structural support.

Now, that support is beginning to roll off.

As options expire, dealer positive gamma exposure declines, making markets more vulnerable to directional swings and volatility. Without those stabilizing flows, investors are increasingly forced to focus on underlying macroeconomic fundamentals — and those fundamentals have become significantly more challenging over the past week. In many ways, Friday’s selling pressure looked less like panic and more like the market suddenly realizing the training wheels had been removed.

The biggest issue remains the bond market.

The U.S. 10-year Treasury yield surged above the psychologically critical 4.50% level Friday morning, climbing toward 4.55%, its highest level since mid-2025. More importantly, technical analysts increasingly believe Treasury yields are breaking out of multi-year consolidation patterns. The 10-year yield recently pushed above resistance near 4.45%, a level that had capped rates for much of the past year. Analysts now argue there is little major technical resistance before yields potentially challenge 5%.

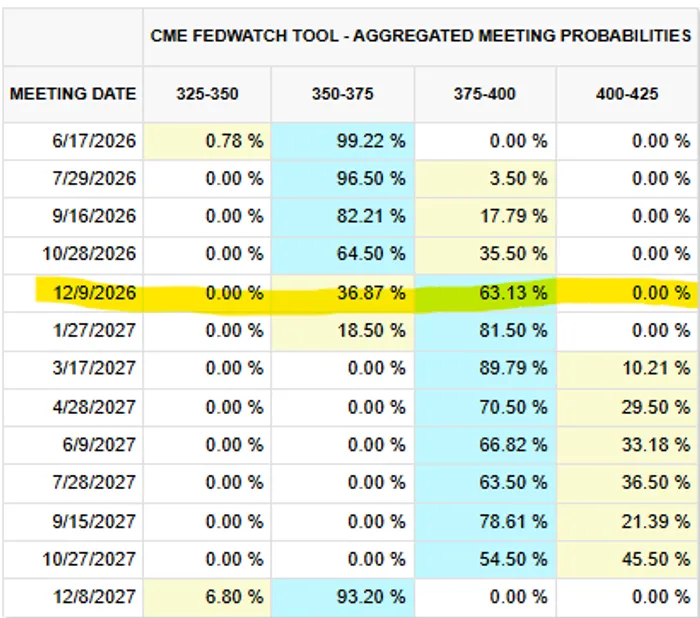

The move has not been isolated to the long end of the curve.

The U.S. 2-year Treasury yield also broke above key resistance near 4.05%, reinforcing the idea that markets are rapidly repricing Federal Reserve expectations. The 2-year yield climbed toward 4.06% Friday as traders increasingly abandoned hopes for rate cuts in 2026 and began discussing the possibility of future hikes instead. According to CME Fed Funds futures, markets are now pricing roughly a 63% probability of at least one rate hike by the December 2026 meeting. Kalshi markets are similarly assigning roughly 35% odds of a Fed hike before 2027.

That repricing has accelerated following a relentless wave of hot inflation data this week.

Tuesday’s CPI report showed headline inflation rising 3.8% year-over-year while core CPI climbed 0.4% month-over-month versus expectations for 0.3%. Wednesday’s producer price report proved even more alarming. Headline PPI surged 1.4% month-over-month versus expectations of 0.5%, while annual PPI inflation accelerated to 6%, the highest level since December 2022. Core PPI excluding food and energy rose 1.0%, more than double consensus expectations.

The troubling part for markets is that inflation pressures no longer appear isolated strictly to gasoline prices.

Energy remains the primary driver, with gasoline prices surging 15.6% during April amid the Iran conflict and disruptions surrounding the Strait of Hormuz. But inflationary pressures are now spreading more broadly into services, machinery, transportation, trade services, and equipment wholesaling. Fed officials have increasingly warned that the risk is no longer simply a temporary energy shock, but rather broader inflation pass-through effects throughout the economy.

Boston Fed President Susan Collins explicitly warned this week that the Fed “might need to raise rates if inflation pressures broaden.” Kansas City Fed President Jeffrey Schmid similarly said persistent inflation remains “the most pressing risk to the economy,” while Minneapolis Fed President Neel Kashkari stressed the Fed is “dead serious” about returning inflation to target. Chicago Fed President Austan Goolsbee acknowledged bluntly that “we have an inflation problem in this country.”

The inflation pressure is not just an American story either.

China reported hotter-than-expected inflation data Sunday night, with producer prices rising 2.8% year-over-year versus expectations of 1.7%, while CPI accelerated to 1.2% from 1.0%. Japan followed with a major upside surprise in wholesale inflation overnight, with April PPI surging 4.9% year-over-year versus expectations near 3.0%. European officials are also beginning to shift more hawkishly. ECB policymaker Joachim Nagel warned markets are “no longer in the baseline scenario” and suggested ECB rate hikes are becoming increasingly likely.

Much of this ties directly back to oil.

For several years now, oil prices and Treasury yields have moved increasingly in tandem. As crude prices rise, inflation expectations increase, bond yields climb, and the dollar tends to strengthen. That relationship has become especially important following the outbreak of conflict involving Iran and disruptions surrounding the Strait of Hormuz. The Trump-Xi summit had created some hope that China might help pressure Tehran toward reopening shipping lanes or stabilizing energy markets. Instead, the summit produced very little concrete progress on Iran, which helped push oil prices higher again Friday.

WTI crude traded back above $100 per barrel while Brent crude pushed toward $109. Analysts increasingly warn that if elevated oil prices persist, inflation will likely continue accelerating into the summer months. The latest Survey of Professional Forecasters now projects first-quarter CPI inflation reaching 6%, versus prior estimates near 2.7%. Headline PCE inflation is projected at 4.5% for Q2.

This creates a particularly difficult environment for equities because rising bond yields directly pressure valuation multiples.

The equity risk premium — essentially the excess return investors receive for owning stocks over risk-free Treasuries — compresses as Treasury yields rise. Put simply, when investors can suddenly earn 4.5%-5% on relatively safe government bonds, richly valued growth stocks become harder to justify. This is particularly problematic for long-duration assets such as semiconductors, AI infrastructure names, and high-growth software companies whose valuations rely heavily on future earnings streams.

That dynamic explains why semiconductors were hit so aggressively Friday despite generally strong earnings results.

Applied Materials (AMAT) delivered a strong beat-and-raise quarter Thursday evening, yet the stock reversed sharply lower Friday morning alongside Nvidia (NVDA), Broadcom (AVGO), Advanced Micro Devices (AMD), and Taiwan Semiconductor Manufacturing Company (TSM). The issue was not fundamentals. It was rates, positioning, and valuation compression.

Ultimately, the market is beginning to transition from an environment dominated by liquidity, dealer support, and AI enthusiasm into one increasingly driven by inflation realities and bond markets. Until oil prices stabilize and yields stop climbing, equities are likely to remain vulnerable to additional pressure — especially with markets now confronting the possibility that the next move from the Federal Reserve may not eventually be a cut, but another hike.