Victoria's Secret shares erupted on June 2 after the lingerie retailer raised its 2026 outlook and reported a 15% first-quarter sales gain, turning a brand-recovery story into a sharper margin question for newly renamed VSXY. Reuters reported the stock jumped about 50% to a record high during Tuesday's session and was last up 40% at $75.61, while the company release showed comparable sales rose 13% and adjusted earnings reached $0.60 a share.

Before the release, the skeptical read was that refreshed marketing and less discounting could lift traffic without durable operating leverage. Company data now challenge that view, but the rally leaves less room for a second-quarter miss, tariff costs or a short-covering fade after Reuters said more than 19% of the float was sold short.

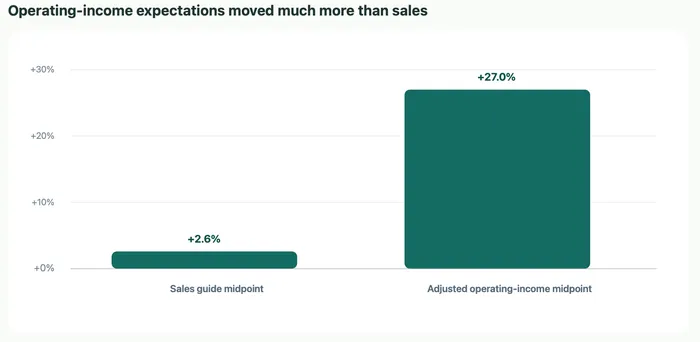

Sales momentum now has profit behind it

Net sales rose to $1.560 billion for the quarter ended May 2, above the company's prior $1.490 billion to $1.525 billion outlook, and total comparable sales rose 13%. Adjusted operating income reached $80 million, more than double the $32 million to $42 million range Victoria's Secret had guided for the quarter, according to the company release.

That mix matters because the turnaround no longer rests only on better store traffic or a refreshed brand image. North America store sales increased 11.3%, direct-channel sales rose 8.4% and international sales jumped 44.9%, giving management more room to argue that product, marketing and channel execution are moving together rather than offsetting one another.

Operating leverage is still a narrower claim than broad demand recovery. The company cited buying and occupancy leverage and SG&A leverage during the quarter, yet the same release warned that consumer confidence, inflation, tariffs, foreign exchange and product acceptance could still pressure results.

A bigger guide makes the stock reaction about leverage

Victoria's Secret lifted its 2026 net-sales outlook to $7.03 billion to $7.13 billion from $6.85 billion to $6.95 billion. The larger move came in adjusted operating income, where guidance rose to $550 million to $580 million from $430 million to $460 million, a change that makes margin delivery the market's main demand on the stock.

Source note. Provider and source are AInvest calculations from Victoria's Secret official FY2026 outlook ranges in the company release

The chart explains why the rally is not just about a sales beat. The sales-guide midpoint increased about 2.6%, while the adjusted operating-income midpoint increased about 27.0%, so the new price reaction is asking whether higher regular-price selling, lower discounts and store leverage can keep carrying profit faster than revenue.

Short interest can amplify the move without settling durability

Reuters said the stock touched a record high, was last up 40% at $75.61 and had more than 19% of its publicly available shares sold short. That combination can turn a guide raise into a violent price move, especially when LSEG estimates cited by Reuters had quarterly revenue at $1.52 billion and adjusted earnings at $0.30 a share before the release.

The short-interest layer cuts both ways. A squeeze can force rapid repricing when results improve, but it can also leave the stock vulnerable if the next update shows the first quarter relied too much on promotions, seasonal demand or cost leverage that cannot repeat through the year.

Tariffs and the consumer split keep the next quarter decisive

Second-quarter guidance is where the new thesis becomes measurable. Victoria's Secret forecast net sales of $1.590 billion to $1.615 billion and operating income of $90 million to $100 million for the quarter ending Aug. 1, against $1.459 billion of sales and $55 million of adjusted operating income a year earlier.

Reuters reported that management expects tariffs to shave about $15 million from current-quarter operating income, even after mitigation efforts, and quoted the company as saying lower-income consumers were pulling back more than higher-income shoppers. That keeps the burden on full-price selling, product mix and expense control rather than traffic alone.

The next report has to separate brand recovery from margin quality

Victoria's Secret also repurchased 2.2 million shares for $100 million at an average price of $45.27 in the first quarter, leaving $150 million available under its authorization, according to the company release. That capital-return marker is useful context, but it will matter less than whether gross margin, inventory discipline and comparable sales can support the new operating-income range.

By the next earnings update, the most useful evidence will be a narrower set of numbers than Tuesday's stock move. Q2 sales need to land near or above the $1.590 billion to $1.615 billion guide, operating income needs to hold the $90 million to $100 million range after tariff costs, comparable sales need to show demand beyond one quarter, and short interest needs to fall without removing the bid from the shares.

The record rally prices a company moving from recovery narrative to operating leverage. It becomes easier to defend if Q2 margins absorb tariffs and the 2026 adjusted operating-income guide holds; it becomes easier to fade if the stock has already pulled forward most of the rerating before the next comp-sales and margin data arrive.