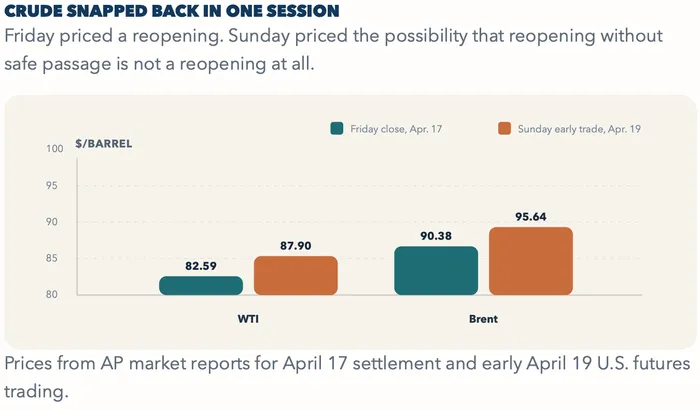

Friday's relief rally made perfect sense for a few hours. After Iran said the Strait of Hormuz was open again to commercial tankers, benchmark U.S. crude fell 9.4% to settle at $82.59 a barrel, Brent dropped 9.1% to $90.38, and the S&P 500 jumped 1.2% to a record 7,126.06. Lower oil meant lower inflation pressure, a friendlier rates backdrop and, at least in theory, an easier earnings season for any business with a fuel bill.

By Sunday, that trade already looked premature. Iran reversed course, fired on several vessels and left tankers stranded again after the Trump administration said a U.S. naval blockade of Iranian ports would remain in force. An hour after trading resumed, U.S. crude was back up 6.4% at $87.90 and Brent had climbed 5.8% to $95.64. That rebound did not fully erase Friday's drop, but it erased the market's neat story that the energy shock had become a one-headline problem.

Source: AP, April 17; AP, April 19.

WHAT FRIDAY MISSED

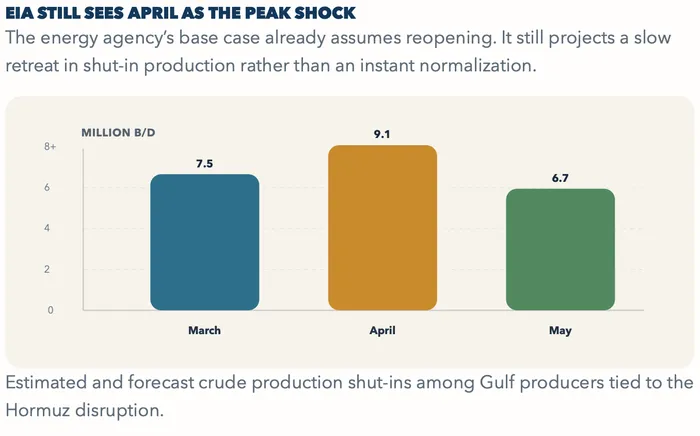

The miss was not in the direction of the first move. If a genuine reopening had taken hold, oil should have fallen and risk assets should have risen. The miss was in assuming that one political declaration changed the physical shape of the bottleneck. EIA's April Short-Term Energy Outlook had already laid out the harder part: even under its base case that conflict does not persist past April, production shut-ins were expected to rise from 7.5 million barrels a day in March to 9.1 million in April, then ease only gradually. The agency explicitly assumes that once flows resume, backlogs, rerouted tankers and the threat of fresh disruptions keep a risk premium embedded in crude through late 2026.

That is why Friday's all-clear looked too eager. EIA's own April forecast still sees Brent peaking at $115 a barrel in the second quarter, averaging $96 in 2026 and only slipping below $90 in the fourth quarter. In other words, the official baseline is not that the world flips from crisis to normal. It is that the world spends months working off the damage of a narrow waterway that was shut, militarized and then nominally reopened before shipping confidence had any reason to normalize.

Source: U.S. Energy Information Administration, April 7, 2026.

The bottleneck is structural before it is financial. The best official baseline for normal traffic is still EIA's March 3 chokepoints analysis, which says 20.9 million barrels a day of oil and 11.4 billion cubic feet a day of LNG moved through Hormuz in the first half of 2025. That is not a live April shipping print, but it remains the latest EIA snapshot of what full-flow conditions looked like before the current disruption. Saudi Arabia's East-West pipeline and the UAE's Abu Dhabi pipeline can bypass only about 4.7 million barrels a day combined, while Iran's own alternative route has effective capacity of around 0.3 million. That means the system does not need a dramatic military escalation to stay stressed. It only needs insurers, vessel operators and navies to disagree about whether passage is truly safe.

This is also where the U.S. market can fool itself. America is not directly hostage to Gulf crude in the way Asia is. In an April 6 analysis, EIA said the United States imported an average 490,000 barrels a day of crude from Middle East Gulf countries in 2025, equal to 8% of U.S. crude imports. But the S&P 500 does not price local barrels. It prices the global benchmark for transport, petrochemicals, aviation, freight, inflation expectations and, by extension, how quickly the Federal Reserve can relax.

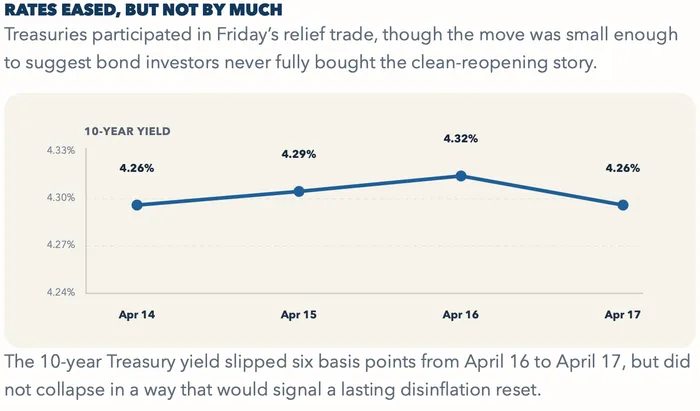

Source: U.S. Treasury Daily Par Yield Curve Rates.

THE TRADE THAT MATTERS NOW

That matters because the market spent Friday buying a chain reaction: open strait, cheaper oil, softer inflation, lower yields, easier Fed, higher multiples. The first link in that chain has already frayed. Treasury data show the 10-year yield fell to 4.26% on April 17 from 4.32% a day earlier, but the move was not large enough to suggest bond investors believed the energy shock had truly cleared. Equities, by contrast, were happy to sprint to a new high.

The better reading is that Friday priced a headline while the weekend restored the logistics. If the strait remains operational only in bursts, the crude market does not need to revisit its war highs to keep pressure on margins and inflation psychology. It only needs Brent to stay well above the levels investors were starting to anchor to before the conflict, while EIA's projected shut-ins and LNG constraints continue to remind the market that supply normalization is a process, not a switch.

The bullish case is not dead. If the ceasefire survives beyond Wednesday, if convoys begin to transit consistently and if insurers and tanker operators start treating Hormuz as reliably open rather than conditionally open, Friday's rally will look early, not wrong. But that case needs evidence in the water, not another announcement on social media. Until then, the market is still trading an energy corridor that has proved easier to declare safe than to make safe.

The easy call was that Friday's reopening statement deserved relief. The harder one, and the one investors now face in the first full trading day after the weekend reversal, is whether Hormuz is moving back toward normal commerce or just generating tradable bursts of optimism. If crude cannot hold its Friday collapse and yields stop extending lower, Wall Street's record high will look less like the start of a durable all-clear and more like a market paying up for a ceasefire it has not actually seen.

Why U.S. Stocks Still Care

- Hormuz handles a fifth of global oil consumption and more than a fifth of global LNG trade.

- Direct U.S. import exposure is modest, but benchmark crude still sets the inflation impulse.

- Friday's equity response leaned hardest into the idea of lower fuel costs and easier rates.