Walmart (WMT) delivered another quarter that reinforced why the company remains one of the strongest operators in global retail, but the market reaction Thursday morning highlighted the growing tension between Walmart’s elite fundamentals and its increasingly stretched valuation. Shares were down roughly 3% in premarket trading following the release despite topping revenue expectations and posting solid comparable sales growth, with investors focusing heavily on softer-than-expected second-quarter EPS guidance, ongoing fuel-cost pressures, and a stock that already trades near 40x forward earnings. Technically, the selloff places Walmart directly near a key test of its 50-day moving average around $127, an important support area after the shares have dramatically outperformed most consumer retail peers over the past year.

From a headline perspective, the quarter itself was solid.

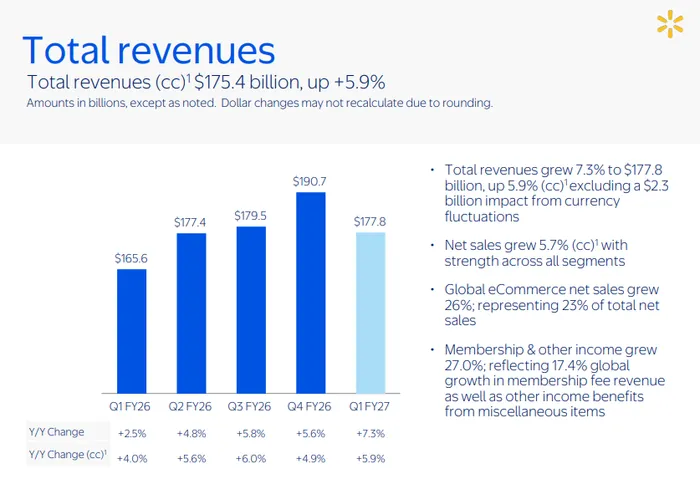

Walmart reported fiscal first-quarter adjusted EPS of $0.66, matching Wall Street expectations, while revenue climbed 7.3% year-over-year to $177.8 billion, comfortably ahead of analyst estimates near $175 billion. On a constant-currency basis, revenue still rose a strong 5.9%, highlighting continued underlying momentum across the business despite macro uncertainty and inflation pressures.

The key operational metric investors were watching closely — U.S. comparable sales — also came in ahead of expectations.

Walmart U.S. comparable sales excluding fuel rose 4.1%, topping consensus estimates closer to 3.8%. Transactions increased 3%, showing consumers are still actively shopping at Walmart despite higher fuel prices and tighter household budgets. Average ticket increased a more modest 1.1%, suggesting Walmart’s growth continues being driven more by traffic gains and market-share expansion rather than pure inflation.

Management specifically highlighted strength from higher-income households, a trend that has become increasingly important for Walmart over the past several years.

Executives said gains were broad-based across major merchandise categories, including grocery, clothing, home goods, and general merchandise — areas that had previously shown signs of weakness as consumers became more cautious around discretionary spending.

One of the biggest drivers of the quarter remained Walmart’s rapidly growing e-commerce and advertising ecosystem.

Global e-commerce sales surged 26%, while Walmart U.S. e-commerce sales also climbed 26%, driven by strong growth in store-fulfilled delivery, pickup, marketplace activity, and advertising revenue. E-commerce contributed roughly 530 basis points to Walmart U.S. comparable sales growth, a massive acceleration compared to prior years.

Advertising was particularly strong.

Global advertising revenue jumped 37%, while Walmart U.S. advertising revenue increased 36%. Walmart Connect, excluding VIZIO contributions, surged 44%. These higher-margin advertising and marketplace businesses are becoming increasingly important because they help offset the structurally lower margins of traditional retail operations.

Membership growth also remained healthy.

Global membership fee revenue rose 17.4%, while Sam’s Club membership revenue increased 5.6%, supported by higher member counts, improved renewal rates, and continued growth in Plus memberships.

Breaking down the major segments, Walmart U.S. remained highly resilient.

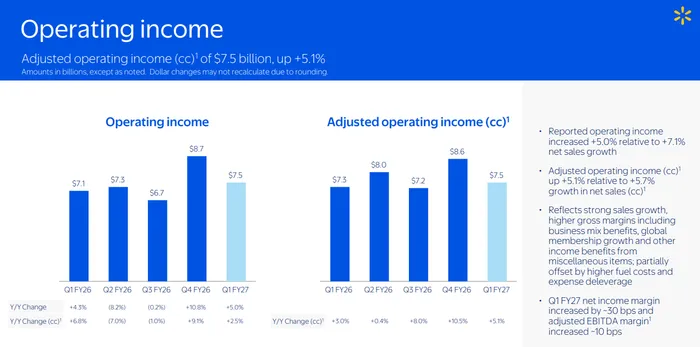

Walmart U.S. revenue increased 4.5% year-over-year to $117.2 billion, while adjusted operating income rose 5.7%. Gross profit rate improved 29 basis points, helped by improved merchandise mix and stronger higher-margin businesses such as advertising and memberships. However, those gains were partially offset by sharply higher fuel costs tied to distribution and fulfillment.

That fuel issue became one of the most important themes in the report.

Management disclosed that operating income growth suffered a roughly 250-basis-point headwind from higher fuel costs across transportation, distribution, and online delivery operations. Rising oil prices increased inventory costs and pressured fulfillment expenses, partially offsetting the benefits of stronger sales and improved e-commerce economics.

Importantly, Walmart noted that tariffs did not materially impact guidance because its outlook does not assume any benefit from potential IEEPA tariff refunds.

Walmart International also delivered another strong quarter.

International revenue increased 18% year-over-year to $35.1 billion, or 10.1% in constant currency. E-commerce sales climbed 27%, while advertising revenue rose 32%, driven largely by continued momentum at Flipkart. Operating income rose nearly 24%, supported by improved e-commerce economics and lower losses within digital operations. Currency fluctuations provided a significant tailwind, positively impacting sales by roughly $2.3 billion and operating income by approximately $200 million.

Sam’s Club continued posting healthy traffic growth as well.

Sam’s Club comparable sales excluding fuel rose 3.9%, while transactions increased 6.2%. However, average ticket declined 2.2%, reflecting moderation in inflation-driven pricing benefits and some mix shift toward lower-ticket grocery categories. E-commerce sales at Sam’s Club still rose 23%, helped by strong pickup and delivery demand.

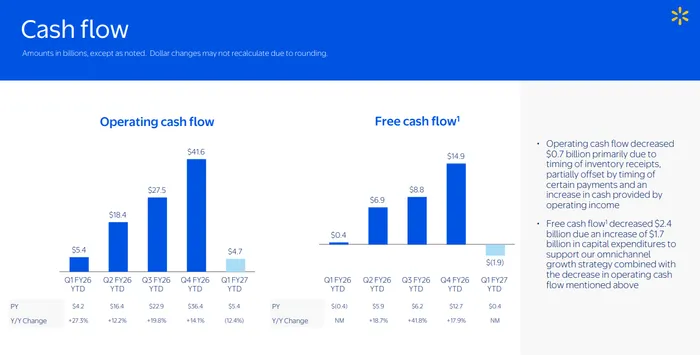

Margins and cash flow, however, were a little more mixed beneath the surface.

Operating income rose 5%, but fuel inflation clearly pressured profitability. Free cash flow also came in negative at roughly -$1.95 billion during the quarter, though management largely attributed that to working capital timing, inventory investments, and seasonal factors. Inventory itself rose 8.9% globally and 8% within Walmart U.S., driven by stronger grocery unit demand, timing of receipts, and elevated fuel values embedded within inventory costs.

The outlook ultimately appears to be what disappointed investors most.

For the fiscal second quarter, Walmart guided adjusted EPS to a range of $0.72-$0.74, slightly below consensus expectations near $0.75. The company also projected Q2 constant-currency sales growth of 4%-5%, modestly below expectations around 5.1%.

At the same time, Walmart reiterated its full-year fiscal 2027 guidance:

Revenue growth of 3.5%-4.5%

Adjusted operating income growth of 6%-8%

Adjusted EPS of $2.75-$2.85

So was the quarter actually weak?

Not really.

In fact, operationally, Walmart likely delivered one of the stronger consumer retail reports of earnings season. Traffic remained strong. Higher-income consumers continued shifting toward Walmart. E-commerce growth stayed explosive. Advertising and marketplace businesses kept scaling rapidly. Grocery trends remained healthy. And management sounded relatively confident about the consumer environment overall.

The bigger issue is valuation.

At roughly 40x forward earnings, Walmart now trades more like a high-growth technology platform than a traditional retailer. That valuation leaves very little room for even minor disappointments around guidance, margins, or macro commentary. Investors increasingly view Walmart as both a defensive consumer staple and a growth platform tied to advertising, logistics, marketplace services, and digital commerce. But maintaining that premium multiple likely requires near-perfect execution every quarter.

The early stock reaction suggests investors may simply be taking profits after another fundamentally strong quarter that failed to dramatically exceed already elevated expectations.

Still, if oil prices stabilize and consumer spending remains resilient, Walmart continues looking well-positioned operationally relative to most of retail. The company’s scale, pricing power, grocery dominance, and rapidly growing higher-margin digital businesses remain major competitive advantages. For now, though, investors appear increasingly focused on whether even Walmart’s outstanding fundamentals can continue justifying one of the richest valuations in the entire consumer sector.