Kevin Warsh’s swearing-in ceremony at the White House was largely ceremonial on the surface, but underneath the symbolism sat a far more consequential reality for financial markets: the Federal Reserve is entering the Warsh era at one of the most hawkish moments of the post-pandemic cycle. The event itself carried historical significance — it marked the first White House swearing-in for a Federal Reserve chair since Ronald Reagan introduced Alan Greenspan decades ago — but the actual policy backdrop surrounding Warsh may ultimately prove far more important than the ceremony itself.

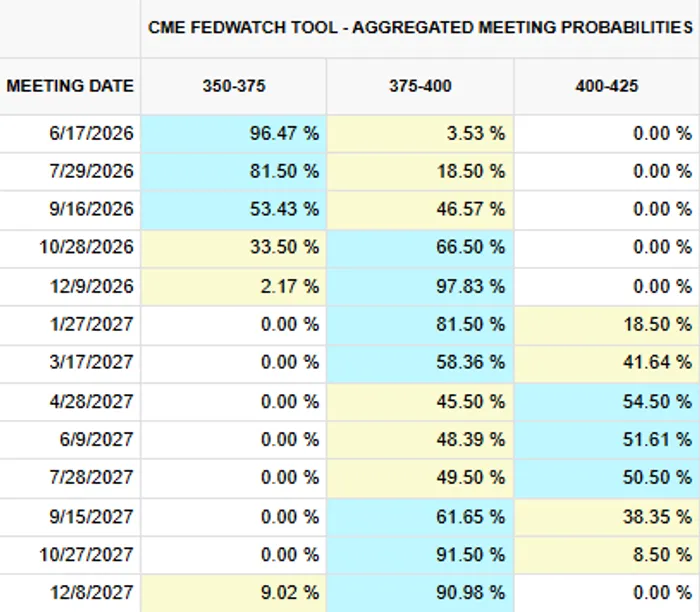

Markets are no longer debating when the first rate cut arrives. Increasingly, investors are debating whether the Federal Reserve may need to hike rates again.

That shift became even clearer this week following a combination of hotter-than-expected inflation data, increasingly hawkish Fed commentary, and the release of FOMC Minutes that revealed growing internal support for removing the easing bias from the Fed’s policy statement. The minutes themselves were initially viewed as a non-event, but the deeper language painted a very different picture. Policymakers repeatedly emphasized inflation persistence, rising commodity costs, and broadening price pressures while expressing relatively little concern about labor-market deterioration.

The key phrase investors focused on was that “many participants” favored removing the easing bias language from the Fed statement. Fed watchers pay extremely close attention to adjectives such as “some,” “several,” “many,” “most,” and “almost all” because they provide clues around the breadth of support within the Committee. “Many” strongly suggests the push toward a more explicitly hawkish policy framework is no longer isolated to a few outspoken members.

Importantly, those minutes reflected thinking before the latest hot inflation reports even arrived.

Since then, both CPI and PPI data have reinforced concerns that inflation progress may be stalling. Energy prices remain elevated, AI-related investment spending continues accelerating, and broader price pressures appear to be spreading through transportation, industrial inputs, and services. The inflation narrative confronting Warsh now looks substantially more difficult than it did even several weeks ago.

Fed Governor Christopher Waller’s comments earlier in the day may have crystallized the issue more clearly than anyone else this week.

Waller explicitly stated that the Fed should remove the easing bias from the statement, though he stopped short of actively advocating for an immediate rate hike. Still, the broader tone was unmistakably hawkish. He noted that inflation risks are becoming more persistent, warned that inflation expectations becoming unanchored would force the Fed to act aggressively, and stated bluntly that “it’s crazy given recent data to be talking about rate cuts in the near future.” This is notable as Waller previously dissented in favor of a rate cut earlier in the year.

Markets reacted immediately.

Fed fund futures traders sharply increased expectations for another rate hike after Waller’s comments, and pricing has now effectively moved toward a 100% probability that rates move higher at some point this year. Just months ago, markets were still expecting multiple cuts during 2026. That psychological shift has happened remarkably quickly.

What makes the current environment especially difficult for Warsh is that nearly every major Fed speaker this week has sounded aligned with the broader hawkish drift.

Chicago Fed President Austan Goolsbee — viewed as one of the more hawkish policymakers — stated that he is now “most attuned to the inflation side of the dual mandate” while acknowledging the U.S. still has a “pretty significant inflation problem.”

Next week’s lineup of Fed speakers only raises the stakes further.

Lorie Logan, Philip Jefferson, Lisa Cook, Austan Goolsbee, John Williams, and Alberto Musalem are all scheduled to speak in the days ahead. Investors will be listening very carefully to determine whether support for removing easing language is continuing to broaden. At this point, the debate no longer appears theoretical. In reality, many policymakers already sound as though the easing bias is effectively gone regardless of whether the formal language has been updated yet.

That creates a potentially difficult backdrop for Warsh personally.

Warsh spoke during the ceremony about reforming the Federal Reserve and modernizing aspects of the institution. President Trump emphasized repeatedly that Warsh should remain independent, even joking directly to him, “don’t look at me, do your own thing.” Warsh himself stressed that inflation can still move lower while growth remains strong.

But reforming the Fed may prove extraordinarily difficult in the near term given current market conditions.

Rate volatility remains extremely elevated, as reflected in the MOVE Index, which continues trading far above pre-pandemic norms. Treasury markets remain highly sensitive to inflation data, geopolitical risks, oil prices, and Fed communication. In that kind of environment, radical policy restructuring or dramatic operational changes become much harder to execute without risking additional instability.

MOVE Chart:

Warsh is also stepping into a central bank where support for easier policy appears increasingly isolated.

The minutes still contained some dovish nuance, with “several participants” acknowledging cuts could eventually become appropriate if energy inflation fades and labor-market weakness emerges. But those voices appear to be shrinking relative to the broader hawkish bloc. Stephen Miran’s earlier dissent in favor of an immediate cut now looks increasingly out of step with the direction of the Committee, particularly after his departure. And Miran has stepped down from the board, taking away a potentially key dovish ally for Warsh.

The biggest near-term test for Warsh may arrive next Thursday with the release of the Core PCE inflation report — the first major inflation data point of the Warsh era.

If PCE comes in hot following already elevated CPI and PPI readings, pressure will likely intensify dramatically around both the Fed’s policy language and the possibility of another hike. Treasury yields would likely move higher, rate volatility could spike again, and markets may begin aggressively pricing the odds of tightening rather than simply removing easing language. If Warsh pushes back against this narrative it could hurt yields even more as the credibility of the Fed would be in question.

Ultimately, the ceremony itself may end up being remembered mostly for its symbolism. The more important story is the policy environment Warsh now inherits. Inflation remains sticky. Oil prices are elevated. Fed officials increasingly sound hawkish. Markets fully price another hike this year. And perhaps most importantly, internal support for removing the easing bias appears to be rapidly becoming the consensus view inside the Federal Reserve itself.

If Warsh eventually wants to steer policy toward cuts, he may first need to convince a Committee that increasingly appears to believe the next move still may need to be higher.