Wells Fargo (WFC) delivered a mixed set of first-quarter results , with earnings modestly ahead of expectations but revenue and net interest income coming in light, leaving investors with a somewhat underwhelming takeaway. Shares are drifting lower in early trade, slipping from $86 to $84, as the market struggles to find a compelling reason to step in aggressively despite broader strength seen in peers like JPMorgan Chase (JPM). From a technical perspective, the stock is now sitting directly on its 200-day moving average, a level that could attract short-term buyers if broader equity momentum continues to improve.

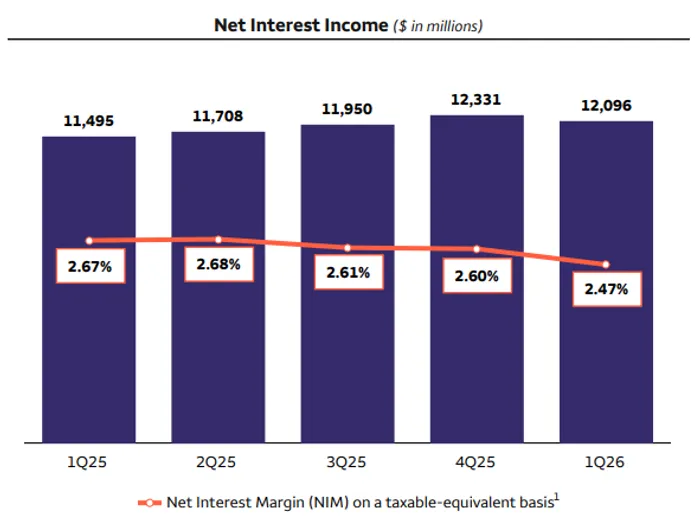

On the headline numbers , Wells Fargo reported earnings per share of $1.60, slightly ahead of the $1.58 consensus, while revenue came in at $21.4 billion, missing expectations of $21.8 billion. Net income was $5.25 billion, and return on equity stood at 12.2%, reflecting a steady but unspectacular level of profitability. The key disappointment was net interest income, which came in at $12.1 billion, below the $12.3 billion estimate, signaling continued pressure from lower rates and balance sheet mix.

That said, underlying trends were more constructive than the headline suggests. Loans grew 10% year-over-year to $996 billion, while deposits increased 6% to $1.4 trillion, indicating solid balance sheet expansion. Net interest income still rose 5% year-over-year, driven by higher loan balances, lower deposit costs, and fixed-rate asset repricing, though these positives were partially offset by the impact of lower rates on floating-rate assets. Noninterest income grew 8%, supported by stronger fee generation in wealth management and improved venture capital performance.

Breaking down the segments, Consumer Banking and Lending delivered steady growth, with revenue up 7% year-over-year. Within that, Consumer, Small and Business Banking rose 9%, driven by higher deposit balances, improved fee income, and stronger customer engagement. Credit card performance was solid, with revenue up 5% on higher loan balances and increased purchase volume, reflecting continued consumer resilience. Auto lending stood out with a 24% increase in revenue, driven by higher originations and balances, while Home Lending declined 9%, pressured by lower mortgage activity and reduced servicing income.

Commercial Banking also showed strength, benefiting from higher loan and deposit balances as well as improved client activity. The segment continues to benefit from Wells Fargo’s focus on deepening relationships and expanding its commercial footprint, though like the rest of the bank, it remains sensitive to broader economic conditions and interest rate dynamics.

The Corporate and Investment Banking segment provided a more mixed picture but still delivered solid growth overall. Revenue increased 4% year-over-year, with Banking revenue up 11% driven by higher lending activity and a notable increase in investment banking fees. Investment banking revenue rose 32% sequentially and 13% year-over-year, reflecting improved capital markets activity and a stronger pipeline. Markets revenue was also strong, rising 19% year-over-year, driven by higher client activity across asset classes, particularly in fixed income and equities.

However, Commercial Real Estate remained a drag, with revenue down 21% year-over-year, largely due to the absence of gains from prior asset sales and continued pressure in that sector. This remains an area of concern for investors, particularly given broader worries about commercial real estate exposure across the banking system.

Wealth and Investment Management was a bright spot, with revenue up 14% year-over-year and client assets increasing 11% to $2.2 trillion. Higher market valuations and strong client engagement drove asset-based fees higher, reinforcing the importance of this segment as a stable, fee-driven growth engine.

On credit, Wells Fargo continues to show relatively stable performance, though there are signs of gradual normalization. The bank reported net charge-offs of $1.1 billion, up modestly year-over-year, with the net charge-off rate holding at 0.45%. Credit costs totaled $1.14 billion, reflecting a modest increase in reserves tied to growth in commercial and auto loans. Importantly, nonperforming assets remained stable at 0.86% of loans, suggesting no meaningful deterioration in asset quality at this stage.

Within consumer credit, charge-offs edged higher, particularly in credit cards, where seasonal trends and higher balances are beginning to show through. Commercial credit trends were also slightly weaker, with higher charge-offs in commercial and industrial loans, though this was partially offset by improvement in commercial real estate exposures.

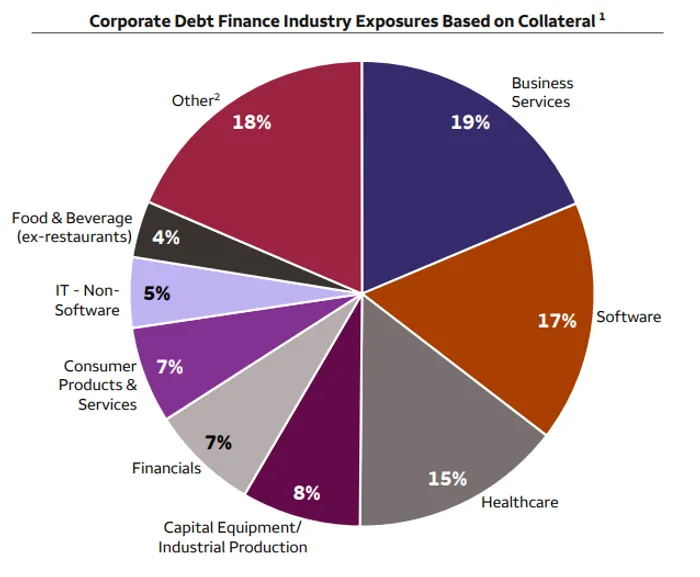

A key area of focus for investors this quarter was Wells Fargo’s disclosure around private credit exposure, particularly given broader market concerns about risks building in that space. The bank reported $36.2 billion of loans tied to private credit funds, representing a relatively small portion of its $1 trillion loan book. Importantly, 98% of these loans are senior secured first-lien positions, providing a strong structural buffer against losses.

The exposure is also diversified across sectors, with 23% tied to business development companies (BDCs), 17% to software, 19% to business services, and 15% to healthcare. This level of transparency is likely to be well received by investors, particularly as concerns grow around private credit, software lending, and the potential for stress in non-bank financial channels. Wells Fargo’s positioning suggests a relatively conservative approach, with strong protections and broad diversification.

From an outlook perspective, the bank maintained its full-year guidance, expecting net interest income of approximately $50 billion and expenses around $55.7 billion. This steady outlook reinforces the idea that Wells Fargo is in a stable, if somewhat slow-growth, phase, with limited near-term catalysts but also relatively contained downside risk.

CEO Charlie Scharf emphasized continued momentum across the business, pointing to strong loan and deposit growth, improving fee income, and solid credit performance. He also noted that while the macro environment remains volatile, underlying consumer and business health remains resilient, though the full impact of higher energy prices and geopolitical tensions has yet to be felt.

Ultimately, Wells Fargo’s quarter reflects a bank that is executing well operationally but struggling to generate excitement in a market that is increasingly focused on growth and upside catalysts. The modest earnings beat was overshadowed by softer revenue and net interest income trends, while the broader macro backdrop remains uncertain.

That said, the stock’s current positioning—sitting at its 200-day moving average—sets up an interesting near-term dynamic. If broader equities continue to squeeze higher, Wells Fargo could attract buyers looking for a laggard with solid fundamentals and defined technical support. For now, however, the market appears content to wait for clearer signs of acceleration before stepping in more aggressively.