Western Digital (WDC) delivered what most investors would typically call a “clean” earnings report—solid beats across key metrics, strong margin expansion, and a bullish outlook—yet the stock is telling a very different story. Shares are down roughly 10% following the release, now testing the psychologically important $400 level after closing near $435 just prior to the print. That kind of price action, especially after a strong report, usually isn’t about what the company did wrong—it’s about expectations that got too far ahead of reality. With the stock up more than 150% year-to-date and nearly 900% over the past year, WDC entered earnings priced for near perfection, and even a strong quarter wasn’t enough to clear that bar.

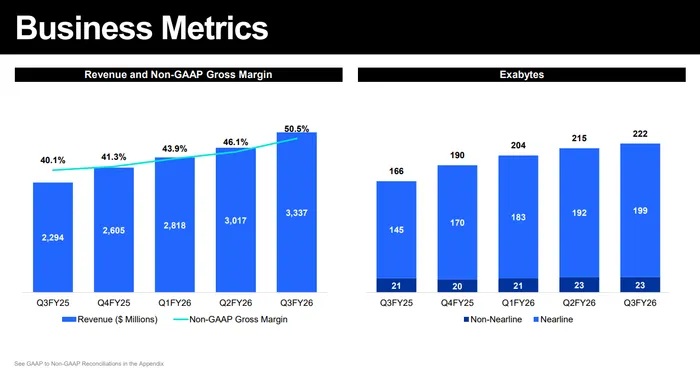

Looking at the headline numbers , the quarter was objectively strong. Western Digital reported adjusted EPS of $2.72, well ahead of consensus estimates of $2.39, while revenue came in at $3.34 billion versus expectations of approximately $3.25 billion. That represents 45% year-over-year revenue growth and nearly double EPS growth from the prior year, underscoring the strength of the current cycle. The company also exceeded its own prior guidance, which had called for EPS between $2.15 and $2.45 and revenue between $3.1 billion and $3.3 billion, suggesting that execution was not only solid but ahead of internal expectations.

Margins were another highlight. Gross margin came in at 50.5% on a non-GAAP basis, expanding more than 400 basis points sequentially and over 1,000 basis points year-over-year. That level of margin expansion reflects both pricing power and a favorable mix shift toward higher-capacity drives, particularly those sold into cloud and hyperscale customers. Operating margins also expanded meaningfully, reaching 38.6%, reinforcing the idea that WDC is benefiting from strong operating leverage as demand accelerates.

The underlying drivers of the quarter are clear and consistent with what we’re seeing across the broader storage and memory complex. Demand tied to artificial intelligence is driving a step-change in data creation, and that data ultimately needs to be stored. As CEO Irving Tan put it, virtually every AI workload—from training to inference to agentic AI—creates persistent data that is stored cost-effectively on hard disk drives. That dynamic is translating directly into higher demand for high-capacity storage solutions, particularly from hyperscalers.

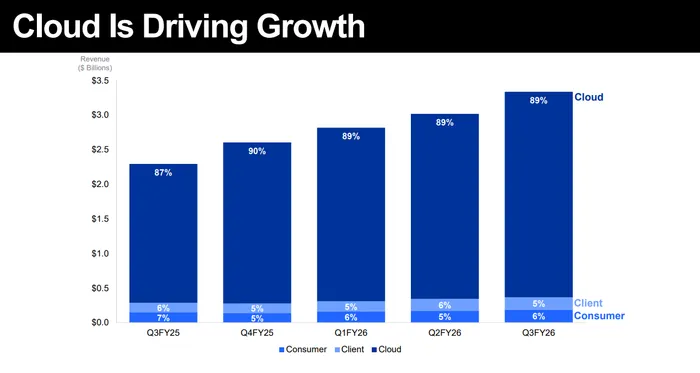

Cloud demand remains the dominant force in the business, accounting for roughly 89% of total revenue, or about $3 billion for the quarter . This concentration highlights both the strength and the risk in the story. On one hand, hyperscaler demand provides significant visibility and scale; on the other, it ties the company’s fortunes closely to the capital spending cycles of a relatively small group of large customers. For now, that demand appears robust, with management pointing to continued strength across AI-driven workloads and long-term expectations for storage demand to grow at a 25% CAGR.

Guidance for the upcoming quarter was also strong, though perhaps not strong enough to satisfy a market that had already priced in continued acceleration. Western Digital expects fiscal fourth-quarter revenue of approximately $3.65 billion, plus or minus $100 million, compared to consensus estimates around $3.46 billion . Adjusted EPS is expected to come in around $3.25 at the midpoint, versus estimates closer to $2.75, while gross margin is guided to 51%–52%, implying further expansion. On paper, that’s a beat-and-raise quarter.

So why is the stock down? The answer lies in the details—and more importantly, in what investors were hoping to hear. While guidance was above consensus, the pace of margin expansion is expected to moderate slightly, with incremental gains not as dramatic as in the prior quarter. Analysts also pressed management on pricing sustainability and whether customers would continue to accept higher prices. Management acknowledged that pricing remains dynamic and tied to long-term agreements, which include both fixed and variable elements. In other words, pricing power is still there, but it may not accelerate indefinitely.

There are also some subtle concerns around supply and capacity. While demand is strong, the company reiterated that it does not plan to significantly increase unit capacity, instead focusing on improving aerial density and transitioning to higher-capacity drives. That strategy supports margins but could limit volume growth if demand continues to outpace supply. Additionally, next-generation technologies like HAMR and ePMR are still in the qualification phase, with full ramps expected over the next 12–18 months. Any delays in those transitions could create execution risk.

Another factor weighing on sentiment is the broader context of the AI trade. Earlier in the week, concerns around slowing growth at AI-related companies triggered a selloff across the sector. While results from peers like Seagate helped stabilize sentiment, investors remain sensitive to any signs that the AI spending boom could slow. In that environment, even strong results can be met with skepticism if they don’t decisively exceed already high expectations.

From a balance sheet perspective, Western Digital is in a much stronger position than it was a year ago. The company used proceeds from monetizing part of its Sandisk stake to reduce debt by $3.1 billion, ending the quarter in a net positive cash position of approximately $450 million. Free cash flow generation was also robust at nearly $1 billion, and management increased the dividend by 20% while continuing to return capital through buybacks. That financial flexibility provides a cushion if the cycle eventually turns.

So, is this a buy-the-dip opportunity? The case for buying here rests on two key arguments. First, the fundamentals remain strong. Demand for data storage is being driven by structural shifts in computing, particularly the rise of AI, and Western Digital is well-positioned to benefit from that trend. Second, the recent pullback appears to be driven more by expectations resetting than by any meaningful deterioration in the business.

At the same time, it’s important to acknowledge that this is no longer an undiscovered story. The stock’s massive run has already priced in a significant portion of the upside, and the bar for continued outperformance remains high. Investors buying here are effectively betting that the AI-driven demand cycle will persist longer than the market currently expects and that Western Digital can continue to execute at a high level.

The bottom line is that Western Digital delivered a strong quarter, but the stock’s reaction reflects a classic case of “good is not good enough” after a massive run. For investors with a longer time horizon, the pullback toward the $400 level likely represents an attractive entry point, provided they are comfortable with the cyclical nature of the business. The fundamentals support the idea that this is a buyable dip—but it’s no longer a low-risk trade.