As the Middle East conflict continues to drive oil prices higher while the labor market remains resilient, U.S. inflation in April is expected to accelerate sharply once again, creating the first major test for incoming Federal Reserve Chair Kevin Warsh.

Although Warsh is viewed as more dovish and aligned with Donald Trump's preference for lower rates, memories remain fresh of how Jerome Powell's premature easing bias during the 2022 inflation surge triggered major market volatility. Markets may still be underestimating the risks today. Whether the latest oil-driven inflation spike proves temporary or evolves into a broader systemic shock capable of reversing the Fed's policy path altogether remains a key concern.

Consensus forecasts call for headline CPI to rise 3.7% year over year — the highest level in nearly three years — while monthly inflation is expected to jump 0.6%.

Core CPI, which excludes food and energy, is projected to rise 2.7% annually and 0.4% month over month. Such a reading would reinforce concerns that rising oil prices are no longer impacting only energy costs, but are increasingly feeding into broader consumer expenses across the economy.

Bank of America rates strategist Mark Cabana warned that markets are underpricing the possibility of renewed rate hikes. During the post-pandemic inflation surge, the Fed's tightening cycle triggered a 25% decline in the S&P 500, and similar risks could emerge again.

Still, Cabana noted that any future rate hikes would likely be more modest than the aggressive post-Covid tightening cycle. Even so, risk assets would likely react negatively.

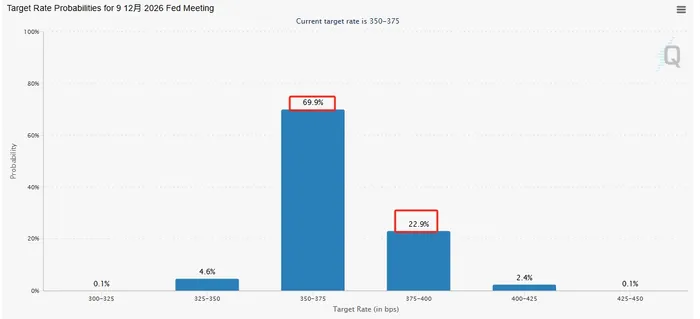

According to FedWatch data, traders are increasingly betting that rates will remain unchanged this year, with roughly a 70% probability of no cuts. Meanwhile, markets now assign a 23% chance of a 25-basis-point hike. Tonight's CPI report could further reshape expectations over whether hikes may return to the table.

Component Outlook

Energy prices remain the primary driver behind the inflation surge.

According to EIA data, the average U.S. retail gasoline price across all grades climbed to $4.236 per gallon in April, up 12% month over month and 28% year over year. Meanwhile, highway diesel prices and jet fuel costs surged 54% and 99%, respectively, from a year earlier.

Those rising transportation and fuel costs are now cascading through the broader supply chain, suggesting the economy may be facing not merely a temporary energy scare, but a broader inflationary shock involving transportation, storage, and replenishment costs rising simultaneously.

Food prices could also begin to accelerate as higher oil and fertilizer costs gradually feed through the system. Although the food component was flat in March, prolonged commodity inflation is expected to place increasing upward pressure on grocery prices over time.

Higher oil prices are also weighing on travel demand and creating structural stress within the auto market.

Research firms J.D. Power and GlobalData estimate the average U.S. new vehicle retail price in April at $45,990, down slightly by 0.5% year over year. However, affordability pressures are intensifying as negative-equity trades climbed to a record 31.3%, while average monthly car payments reached $812.

The used-car market is also cooling. The Manheim Index showed wholesale used vehicle prices rose 1.8% year over year in April but declined 1.6% from the previous month.

Housing — the largest component of CPI — continues to reflect a "two-speed economy."

According to Zumper's national rent report, the median U.S. one-bedroom rent rose 0.4% month over month to $1,508 in April, while two-bedroom rents climbed 0.8% to $1,895.

However, rental trends vary dramatically by region. In San Francisco, rents surged 20% year over year as the AI boom fueled another wave of strength across Silicon Valley housing markets. By contrast, rents in areas such as Los Angeles fell 4% amid oversupply conditions.

Overall, the upcoming inflation report is still expected to be heavily driven by higher oil prices. However, the more important question is whether rising commodity prices are now spilling over into broader day-to-day consumer costs — a sign that inflationary pressures may become far more entrenched.