Nvidia heads into its fiscal first-quarter earnings report with expectations running extraordinarily high, as investors look beyond another likely blockbuster quarter and focus on whether the AI giant can sustain its historic growth trajectory into 2027 and beyond.

Options markets currently imply Nvidia shares could move approximately 6.5% in either direction following results, translating into a potential market capitalization swing of roughly $350 billion to $355 billion. That magnitude exceeds the total valuation of most companies in the S&P 500 and highlights Nvidia's growing influence over global markets.

Wall Street currently expects Nvidia to generate roughly $78.5 billion in fiscal Q1 2026 revenue, up 78% year over year, driven overwhelmingly by continued strength in its Data Center business. Consensus estimates suggest Data Center revenue could reach $72.8 billion, reflecting surging demand from hyperscale cloud providers and enterprises aggressively expanding AI infrastructure.

The segment remains the central pillar of Nvidia's AI dominance as companies continue shifting toward accelerated computing systems powered by GPUs. However, while demand remains robust, investors are increasingly focused on what comes next.

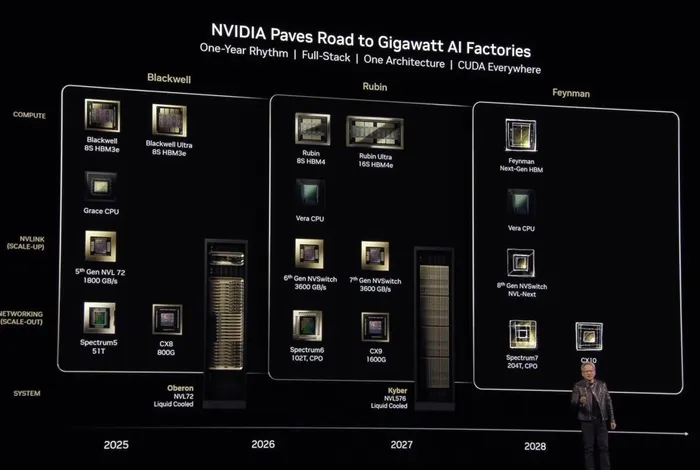

Much of the attention now centers on Nvidia's flagship and next-generation AI platforms, Blackwell and Rubin, which management believes could dramatically improve computing efficiency while lowering operating costs for customers. Yet questions remain around adoption timing, supply constraints, and the total addressable market.

Blackwell remains particularly critical to Nvidia's longer-term narrative. Consensus projects Blackwell revenue climbing from approximately $86.4 billion last year to $137 billion this year, helping drive Data Center revenue expectations toward $343.4 billion for fiscal 2027. Rubin is expected to begin contributing revenue next quarter, with analysts currently forecasting roughly $38.2 billion in annual revenue contribution.

Profitability expectations have also strengthened substantially.

Consensus gross profit forecasts for Nvidia's Data Center segment have risen roughly 34% over the past year to approximately $56.4 billion, supported by sustained AI demand. While gross margins are expected to moderate slightly from peak levels near 78% toward roughly 76.3%, analysts anticipate operating leverage continuing to expand profitability, with operating margins projected to rise to 66.1% by fiscal 2027.

Those projections help explain why Nvidia currently trades at roughly 20 times projected fiscal 2027 earnings, despite ongoing concerns surrounding competition, AI spending durability, and potential margin compression.

Still, investors appear increasingly unwilling to reward Nvidia merely for beating estimates.

After multiple quarters of delivering outsized earnings surprises, markets are now demanding evidence that Nvidia's AI leadership can remain intact well into the Rubin generation and beyond.

Among the bulls is Morgan Stanley analyst Joseph Moore, who remains highly optimistic on Nvidia's trajectory.

"We think the quarter will be a positive step toward a stock rerating," Moore said.

However, he added a key caveat."Nvidia can only do so much on a Q1 earnings call to ease concerns on longer-term debates."

Moore expects Nvidia to continue its familiar beat-and-raise pattern, forecasting roughly a $3 billion revenue beat alongside guidance approximately $4 billion above consensus.

More importantly, Moore believes Wall Street may still be underestimating Nvidia's longer-term AI opportunity.

Regarding Nvidia's ambitious target of reaching $1 trillion in AI accelerator revenue between 2025 and 2027, Moore estimates total Data Center revenue could ultimately exceed current expectations substantially.

Consensus currently forecasts roughly $785 billion in total Data Center revenue during calendar years 2026 and 2027. Moore, however, projects approximately $884 billion, rising to roughly $1.07 trillion across 2025 through 2027.

"We think consensus is likely to move much closer to our estimates as Nvidia reaffirms their visibility to those numbers," Moore said.

Supply limitations involving advanced wafer capacity, DRAM availability, and power infrastructure constraints could challenge Nvidia's ability to fully capitalize on AI demand growth.

Competition also continues building from custom AI accelerators and application-specific integrated circuits (ASICs), though Moore believes concerns over market share become less significant if Nvidia's broader AI revenue ambitions materialize.

"All debates we think can turn more in Nvidia's favor as Rubin begins to ship in volume later this year and is key to our positive view on the risk-reward," Moore added.

China could become both an uncertainty and a tremendous growth engine.

Nvidia has received licenses from the U.S. government to sell H20 chips, but approval from Chinese regulators remains uncertain as China continues fostering domestic semiconductor suppliers. President Trump's talks with Chinese President Xi produced no immediate breakthrough that would allow Nvidia broader access to the Chinese AI chip market.

Nvidia once commanded roughly 95% of China's advanced AI chip market but has effectively fallen to near zero following export restrictions. The company currently guides for little contribution from China, leaving the country as a potentially massive upside opportunity if regulatory and geopolitical conditions improve.

Nvidia shares have already climbed roughly 19% this year, further cementing its role as the central beneficiary of the artificial intelligence investment boom.