Taiwan Semiconductor Manufacturing Company—widely seen as the key gatekeeper of the AI supply chain—reported first-quarter results that once again smashed expectations, with guidance turning even more robust.

For the first quarter, the chip foundry reported revenue of $35.9 billion, up 41% year over year (35% in New Taiwan dollar terms) and 6% quarter over quarter, exceeding its prior guidance ceiling of $35.8 billion. Net income rose to $18.1 billion, marking a 65% annual increase (59% in NT$ terms).

Pricing power continued to strengthen. Gross margin reached 66.2%, up 2.9 percentage points from the previous quarter. The expansion was driven by early volume production of 2nm technology, rising memory chip prices, and sustained AI demand, further reinforcing TSMC's competitive moat.

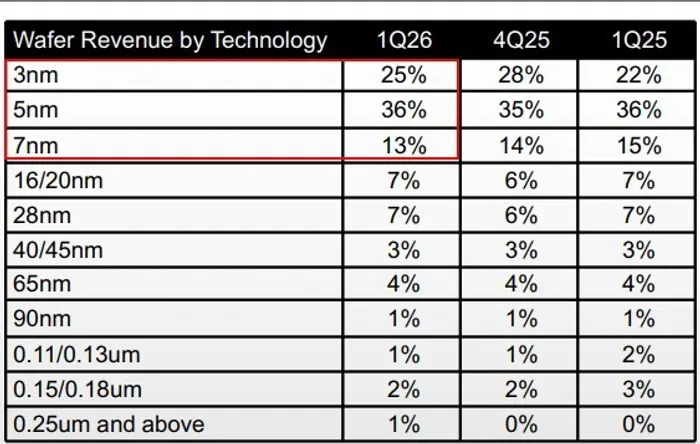

While cyclical softness in consumer electronics persisted, AI demand remained exceptionally strong. Revenue contribution from 3nm chips reached 25%, down 3 percentage points quarter over quarter but up 3 points year over year. Seasonal weakness following the holiday cycle—particularly for devices such as smartphones—was partly offset by ramping production tied to next-generation AI architectures.

Meanwhile, 5nm chips, a core node for AI workloads, accounted for 36% of revenue, up 1 percentage point quarter over quarter and flat year over year. Revenue contribution from 7nm chips came in at 13%, down 1 percentage point quarter over quarter. Combined, advanced nodes (3nm, 5nm, and 7nm) contributed 74% of total revenue, down slightly from the prior quarter.

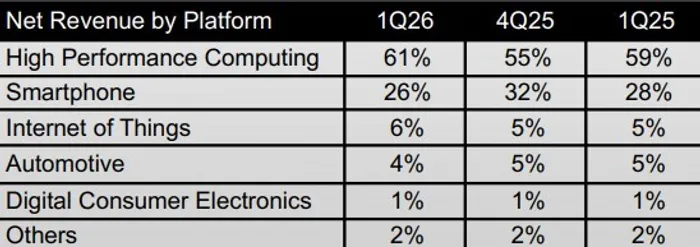

By platform, high-performance computing (HPC) remained the dominant growth driver, accounting for 61% of revenue, up 6 percentage points sequentially. Demand from AI-related applications—including GPUs, custom accelerators, and advanced memory integration—continued to scale rapidly, positioning TSMC as a long-term beneficiary of the AI buildout.

Smartphone-related revenue declined 6 percentage points to 26%, reflecting cyclical headwinds, though these were largely offset by sustained AI demand. Internet of Things (IoT) and automotive segments contributed 6% and 4% of revenue, respectively.

TSMC expects second-quarter revenue to reach $39 billion to $40.2 billion, setting another record. At the midpoint, this implies 10% quarter-over-quarter growth and 32% year-over-year expansion. The company also forecasts full-year revenue growth of more than 30% in U.S. dollar terms.

Gross margin for the second quarter is projected at 65.5% to 67.5%, reflecting continued strong pricing power.

To meet surging AI demand, TSMC is ramping up investment. The company now expects 2026 capital expenditures to reach the high end of $52 billion to $56 billion. Its 2nm process has entered volume production, while 3nm capacity is being expanded aggressively. At the same time, mature-node capacity is being scaled up at its facilities in Japan and Germany. The next-generation A14 (1.4nm) process is slated for mass production starting in 2028.

Regarding potential supply chain disruptions from geopolitical tensions in the Middle East, TSMC said prices for certain chemicals and gases may rise, though it is too early to quantify the impact. The company maintains safety stockpiles of key inputs such as helium and hydrogen, and expects no near-term disruption to raw material supply.

TSMC's results underscore that the AI narrative is not only intact but accelerating. With surging demand, expanding margins, and aggressive capacity buildout, any discussion of a near-term peak appears premature. AI is set to remain the defining growth driver throughout the year.